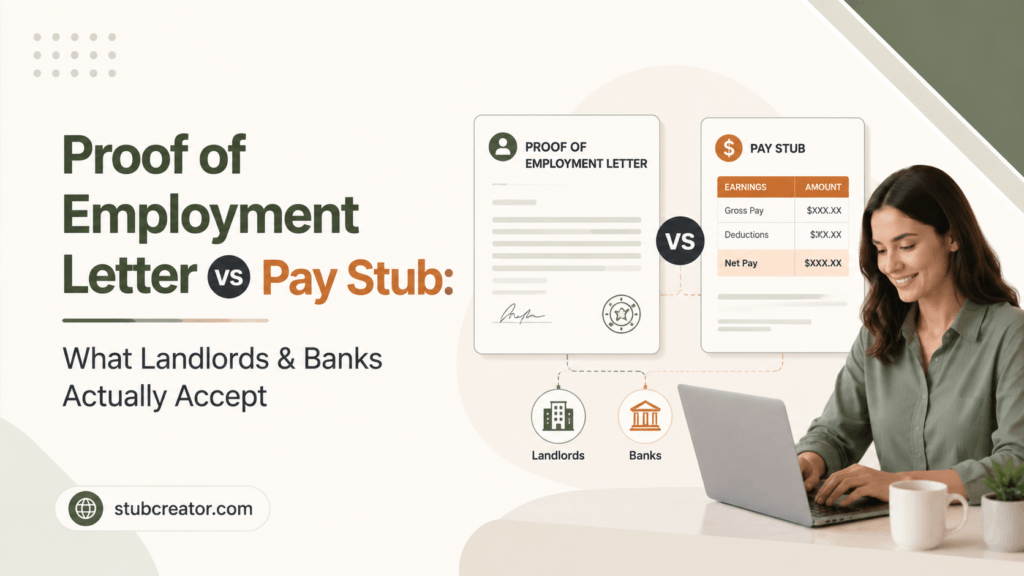

When you apply for an apartment, a mortgage, or a personal loan, the proof of employment letter is one of the fastest ways to provide proof of income. You are aware that you have a job. You even know that your income is enough. But when the landlord, bank, or lender requests a particular document, you don’t know if you should give them your proof of employment letter, your latest pay stub, or maybe both.

Whether you use the employment verification letters or a paystub, your main aim is to get the income verification! Here in this guide, we will help you to decide in which scenarios letters are good or pay stubs are good to show! However, a reliable free pay stub generator tool helps you to create a paystub to show anytime, anywhere.

What is an Employment Letter for Apartment?

A proof of employment letter, which is also known as a verification of employment letter (VOE or EVL), is a formal document that is given to you by your employer. Most of the time, it is the HR or payroll departments that issue the letter confirming that you are actively working for the company. The employment details include:

- Your full name and job title

- Your start date and employment status

- Your salary information or hourly wage

- The name, address, and contact information of the employer

- A signature from an authorized HR representative or manager

- Company letterhead

When is a Proof of Employment Letter Most Useful?

There are several scenarios where you find the employment verification letters most useful. Here we mentioned some:

- You’ve just started a new job and don’t yet have pay stubs

- You’re applying for a visa or a government benefit

- A landlord or lender wants third-party employer confirmation

- You’re transitioning between jobs and need to bridge the documentation gap

As of 2026, over 20 states have active salary history ban laws that prohibit employers from asking job applicants about their previous compensation.

These states include Alabama, California, Colorado, Connecticut, Delaware, Hawaii, Illinois, Maine, Maryland, Massachusetts, Nevada, New Jersey, New York, North Carolina, Oregon, Pennsylvania, Rhode Island, Vermont, Virginia, Washington, and others. Virginia is the newest addition, with its ban on private employers taking effect July 1, 2026.

Note that these restrictions apply specifically to the hiring process; they do not prevent employers from including current salary details in employment verification letters issued to existing employees for rental or loan applications.

What is a Pay Stub as Proof of Income?

A pay stub as proof of income is a document that is generated via payroll or paystub generator tool, which is attached to your paycheck that details your earnings for a specific pay period. It includes additional information beyond the employment letter:

- Gross pay

- Net pay

- Federal, state, and local tax withholdings

- FICA deductions

- Year-to-date totals

- Pay period dates and pay frequency

Pay stubs provide older earnings figures as opposed to merely confirming cutting-edge popularity. This makes them more effective at verifying consistent benefits, which is what lenders and homeowners care about the most.

What Do Landlords Accept As Proof of Income?

Here we gave the list of what Landlords accept as proof of income documents:

- Pay Stubs: The first preferred document for income verification. Most landlords ask for 2–3 recent stubs. They use them to apply the 3x rent rule (gross monthly income ≥ 3× rent) and verify income consistency.

- Proof of Employment Letter: Useful for new hires who don’t have stubs yet. Usually accepted as a bridge document, with stubs expected within 30–60 days. If previously worked, then work history, work status, and some specific details are added.

- Bank Statements: 2–3 months of bank statements are standard. Landlords cross-check deposits against pay stubs’ net pay to confirm authenticity.

- Tax Returns: Common for self-employed, freelancers, or gig workers. Usually paired with bank statements for a complete picture.

- Offer Letter: Accepted as temporary proof for new hires, provided it clearly states the start date, position, and salary.

- Government Benefit Award Letters: For retirees or disability recipients, confirm the fixed monthly income amount.

- 1099 Forms + Invoices: For contractors and freelancers, often requested alongside bank statements or tax returns.

- Direct Digital Income Verification: Increasingly used by larger property managers and landlords in 2026. Instead of collecting physical documents, landlords can securely access a verified snapshot of an applicant’s income directly from their bank account data without seeing full account details.

This method cross-checks income deposits in real time and can replace or supplement pay stubs and bank statements in the screening process. If your landlord uses this method, traditional paper documents may not be required at all.

Major Differences: Employment Letter vs Pay Stub

| Factors | Proof of Employment Letter | Pay Stub |

| Issued by | Employer | Payroll system |

| Shows income history | No | Yes |

| Verifies employment status | Yes | Indirectly |

| Useful for new hires | Yes | Limited |

| Used for a mortgage | Required often | Required always |

| Used for rental applications | Lower | Higher |

| Self-employed applicants | Not applicable | Not applicable |

What Banks and Lenders Accept: Higher Bar?

Banks, credit unions, and mortgage lenders operate under substantially more stringent earnings verification standards than homeowners. Their needs are constitutively controlled through Fannie Mae, Freddie Mac, and FHA signals, as their documentation requirements are established and non-negotiable.

For Mortgage Applications

Mortgage lenders generally require each file, not one or a choice. According to current lending guidelines, a prevailing W-2 employee applying for a conventional mortgage may wish to provide:

Most recent 30 days of pay stubs.

Note: Pay stubs for mortgage qualification must show more than just current pay period earnings; they must include complete year-to-date (YTD) totals.

Lenders use YTD figures to calculate stable monthly income for underwriting. If your pay stub lacks YTD data (e.g., it is handwritten or employer-typed without totals), the lender will require supplemental documentation, such as a written VOE or bank statement review.

- Verification of employment

- W-2 forms from the last two years

- Two months of bank statements

- Federal tax returns

The pay stubs verify both the present earnings and the income stability over the year-to-date period. Most employment verification letters offer assurance that the borrower is still working at the company at the time of closing, not merely at the time of application.

This difference is hugely significant in the underwriting process. Under current Fannie Mae guidelines, lenders are required to conduct a verbal Verification of Employment (verbal VOE) within 10 business days before the note date; a step formally known as the Pre-Closing Verification (PCV). This confirms the borrower is still employed between application and funding. Lenders may also fulfill this requirement through third-party verification providers such as The Work Number (Equifax) or Experian Verify, as long as the data comes directly from the employer’s payroll system to the lender.

For Personal Loans and Auto Loans

Personal lenders require less documentation than mortgage insure but most still ask for:

- Two recent pay stubs

- A bank statement showing regular income deposits

- A proof of employment letter

When Lenders Accept One Without the Other?

Sometimes, lenders might accept an employment letter without the borrower providing pay stubs, for example, in scenarios of new hires when the noncontingent offer letter clearly states the start date, position, and salary. Still, after the borrower starts their job, a lender will normally ask for at least one pay stub before closing.

Then again, pay stubs on their own are usually enough for personal loans and rental applications for employees with a steady income history. In the case of mortgage applications, the employment letter is rarely optional.

Red Flag That Trigger Scrutiny

Whether you’re submitting a proof of income document, landlords watch for these warning signals:

On Pay Stubs

- Missing pay periods

- YTD totals that don’t align with the stated pay rate and frequency

- Employer details that don’t match publicly listed company information

- Unusual deduction patterns or zero tax withholdings

- Font inconsistencies or formatting errors

On Employment Letters

- Missing company letterhead or unauthorized signatures

- Vague salary language

- No contact information for employer verification

- Letters written by an interested party

More and more, landlords who check the authenticity of pay stubs through a comparison with bank statements are doing so during the process of verification. The net pay mentioned on the pay stub ought to be nearly the same as the amounts of deposits in the account. Mortgage lenders resort to third-party payroll data providers when confirming the borrower’s income directly from the source. This makes the act of forgery very hazardous, both for the risk of documentary fraud and the arising legal consequences.

Note: You can make your own pay stub by using the free pay stub template with calculator, without worrying about proof of income.

How to request a proof of employment letter?

If you need a verification letter, below is what to do:

- Contact your HR Department directly: Most process requests via HR platforms like ADP or Gusto.

- Specify the motive: Whether it is a rental or personal loan, so HR includes the right details.

- Set a deadline: Digital HR systems turn these around in 1 business day; a manual HR department can take up to 7 days.

- Review the letter: Confirm your name, job title, and start date are accurate before submitting it to a landlord.

- Submit the right channel: Most lenders accept employment verification letters through a secure online portal or directly through a loan officer.

If there is a delay, ask your lender whether or not pay stubs or verbal verification can serve as an instant replacement even while waiting for an authenticated letter.

Which Documents Should You Submit?

Below is what documents you should submit:

- Applying for an apartment and have been at your job for 3+ months: Submit 2-3 current pay stubs as proof of income for an apartment. If the landlord specifically requests it, add an employment letter.

- You just started a new job: Present your signed providing letter or corporate verification letter. Inform the owner that pay stubs are approaching and arrange for them to be delivered in 30–60 days.

- You’re applying for a mortgage: Submit every 30 days of pay stubs and a proper verification of employment letter. Have your W-2s for the past two years prepared as nicely as possible.

- You’re a freelancer: Neither traditional employment letters nor paychecks apply. Use tax returns, bank statements, 1099s, and P&L renderings. A paystub generator can help document your earnings in a layout based on the prevalence of many homeowners.

- You’re applying for a personal loan:2-3 recent pay stubs are sufficient. An employment verification letter adds credibility if your pay history is short.

Key Takeaways

The main difference really boils down to this: a proof of employment letter verifies who your employer is and how much you earn; a pay stub shows that you receive your salary regularly. Most lenders require both, and you can’t blame them. A combination of these documents gives a full picture of your financial stability.

For example, if you are getting ready to apply for a lease or a loan, you should start collecting your documents well before the landlord or lender asks for them. Pick up your latest pay stubs, order your employment verification letter from your HR department at least a couple of days before the time you need it, and you should keep your bank statements and tax documents organized and ready to go. The people who get approved quickly and easily are really those who consider paperwork as part of their preparation rather than as a barrier.

If you’re missing recent pay records, a reliable check stub maker can help you create professional pay stubs that accurately reflect your income and employment details.

FAQs

1) How do I get a proof of employment letter?

You can get a proof of employment letter by reaching out to your HR department or direct manager. Make a formal request that clearly states what details the letter should contain, and also provide the recipient’s exact contact information or mailing address.

2) How do you write a proof of employment letter?

An employment verification letter is used to verify someone’s current or previous job status. It is most often required when a person is renting an apartment, applying for a mortgage, or applying for a visa. Besides, it has to be printed on the company’s official letterhead and signed by an authorized person.

3) What is an example of proof of employment?

W-2 form, tax filings, or bank statements.

4) Can I use a W-2 as proof of employment?

While no federal code limits employers from asking for a W-2, some states have legal guidelines that prohibit the exercise or prohibit basing employment selection on data you might discover within a W-2.

5) Can I make my own employment verification letter?

Of course, you can write the letter on your own, but it has to be examined and signed by a person who has the authority. A letter that is signed by oneself is usually not accepted by banks and landlords because it needs to be officially verified by an employer.

6) What is a good document for proof of employment?

The employment verification letter, additionally referred to as the certificate of employment, is the proper document that confirms current or previous employment with the agency. Often, teams of people harass those letters with the request of the worker in the third celebration.

7) What are the types of proof of employment?

Pay stubs and different pay facts that show the worker’s earnings over an extended period of time; references in the field of modern-day employment of human beings, or contracts and other signed documents.

8) Who can request proof of employment?

Several parties may request income verification from your employees, including lenders such as auto, mortgage, and personal loan lenders, homeowners, and government agencies that run public assistance programs.

9) What is sufficient proof of employment?

If you’re preparing a letter for verification of employment, make sure you mention the employee’s position, length of service, and remuneration details. In case the purpose of the employment verification is related to the employee’s skills, you can also attach the list of duties the employee performed as a reference.

10) How do I ask for a letter of proof of work?

One way to go about it is to send a brief message such as: Hi [HR REPRESENTATIVE NAME], I am reaching out to ask for a job confirmation letter, as it is necessary for me to submit it with my [mortgage, car loan, rental application, etc.]. Please make sure that the letter contains what comes next details: [list requested information].