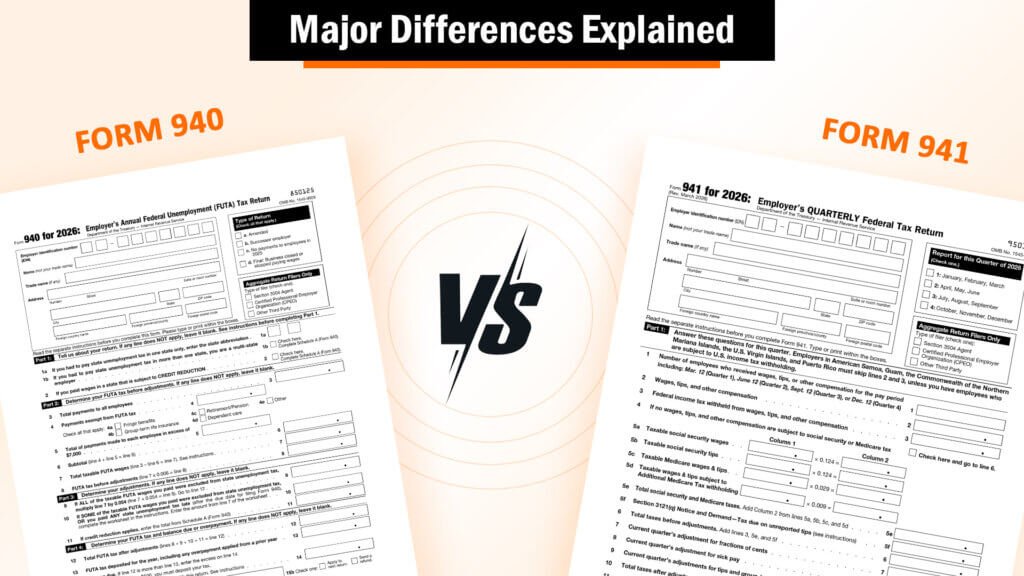

If you run a business with employees, two IRS forms will define your payroll tax compliance calendar every single year: Form 940 and Form 941. While both deal with employment taxes, they serve very different purposes, follow different filing schedules, and carry different consequences if mishandled.

Even if you use a paystub generator free tool to generate a professional paystub or simplify wage calculations and paycheck documentation, understanding how these two forms function is essential to staying compliant and avoiding costly penalties.

Whether you’re a first-time employer trying to understand your obligations or a seasoned payroll professional brushing up on the latest IRS changes, this guide gives you a complete, authoritative breakdown of 940 vs 941. This blog includes definitions, differences, filing deadlines, instructions, where to mail each form, and the newest 2026 updates you cannot afford to miss.

What Are 940 and 941 Forms?

At their core, both Form 940/941 employer tax returns are filed with the IRS, but they report entirely different types of tax.

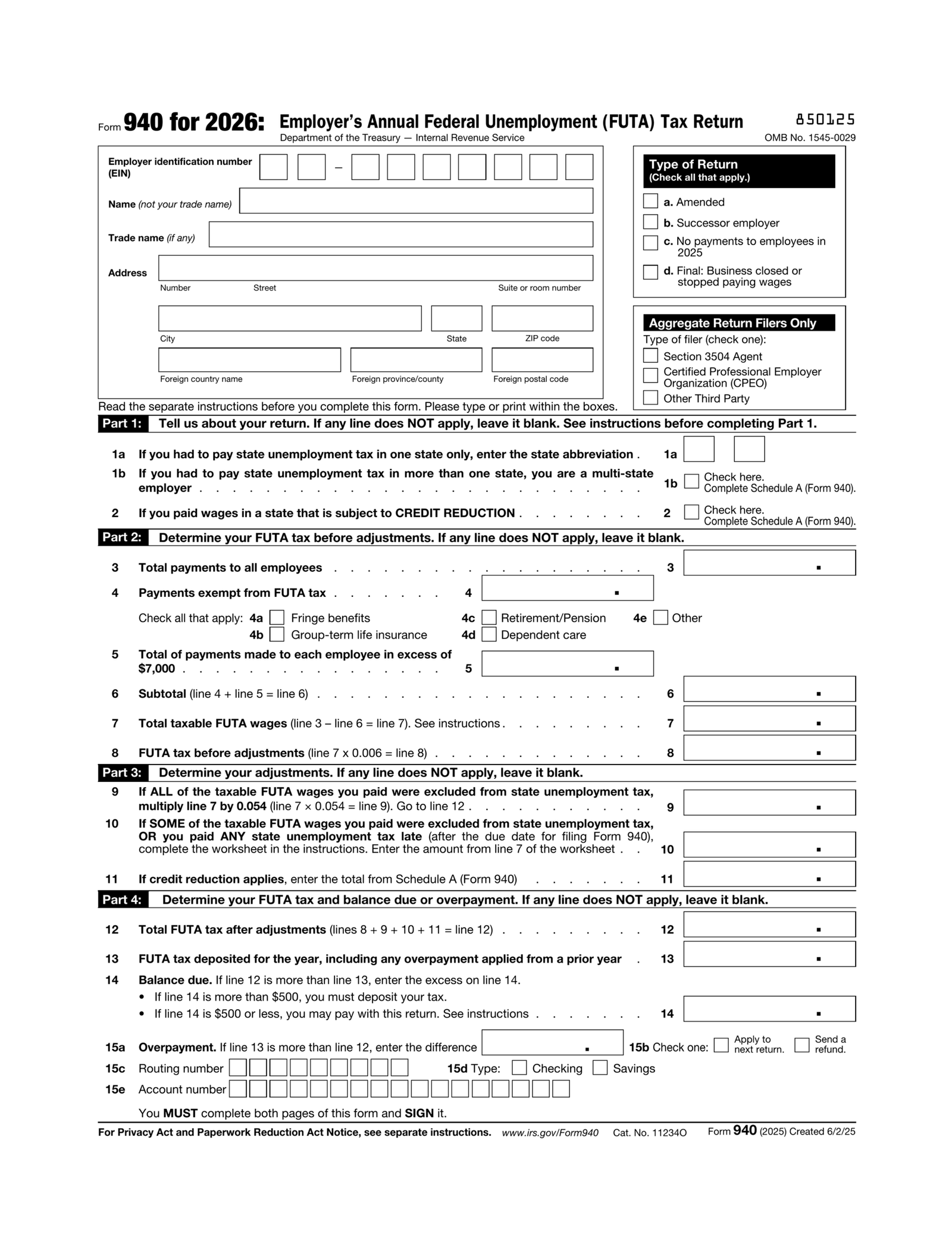

Form 940 is the Employer’s Annual Federal Unemployment Tax Return Form.

It reports the Federal Unemployment Tax Act taxes that an employer owes. These taxes fund unemployment benefits for workers who lose their jobs. Importantly, FUTA is paid solely by the employer; it is never withheld from an employee’s paycheck.

Form 941 is the Employer’s Quarterly Federal Tax Return Form.

It reports three things:

- Federal income tax withheld from employee wages,

- The employee’s share of Social Security and Medicare taxes,

- The employer’s matching share of FICA taxes.

What is Form 940 Used For?

Form 940 exists to calculate and report your business’s FUTA tax liability for the entire year. The FUTA tax rate is 6% on the first $7,000 of each employee’s wages, giving a maximum gross FUTA tax of $420 per employee annually.

However, most employers qualify for a credit of up to 5.4% if they pay into a state unemployment insurance fund in full and on time, reducing the effective FUTA rate to just 0.6% or $42 per employee per year.

However, most employers qualify for a credit of up to 5.4% if they pay into a state unemployment insurance fund in full and on time, reducing the effective FUTA rate to just 0.6% or $42 per employee per year.

What Is Form 941 Used For?

The Form 941 is your quarterly payroll tax report. It tells the IRS how much federal income tax you withheld from employee paychecks and how much Social Security and Medicare tax you and your employees owe together.

The form covers the following:

- Federal income tax withheld from employee wages.

- Employee Social Security tax.

- Employee Medicare tax.

- Employer’s matching share of Social Security and Medicare.

For 2026, the IRS updated the Social Security wage base limit to $184,500, up from $176,100 in 2025. Medicare has no wage base limit. These numbers matter because they directly affect what you report on Form 941 each quarter.

Who Must File Form 940?

According to the IRS instructions for Form 940, you are required to file if either of the following conditions applies:

- Employers who paid $1,500 or more in wages in any calendar quarter.

- You had one or more employees for at least part of a day in 20 or more different weeks during the year.

- Household employers do NOT file Form 940. They report FUTA taxes using Schedule H (Form 1040) instead.

- If you paid $20,000 or more in cash wages to farmworkers in a calendar quarter, or employed 10 or more agricultural workers during 20 weeks, filing is required.

Who Must File Form 941?

Most private-sector employers who pay wages and withhold taxes must file Form 941 quarterly. To ensure accurate reporting, many businesses use a free paystub generator to calculate wages, deductions, and withholdings before submitting their quarterly return.

There are limited exceptions:

- Seasonal employers with no tax liability for an entire quarter may skip filing that quarter.

- Small employers with an annual payroll tax liability of $1,000 or less may file Form 944 annually. This is the key distinction in the Form 944 vs 941 comparison.

- Agricultural employers file Form 943 instead.

Who Is Exempt from Filing Form 940?

The following groups are exempt from filing Form 940:

- Tax-exempt non-profit organizations.

- Household employers report FUTA taxes using Schedule H (Form 1040) instead of filing Form 940.

- Agricultural employers who paid less than $20,000 in farmworker wages annually and employed fewer than 10 farmworkers for 20+ weeks.

- State and local government employers.

- Federally recognized Indian tribal government employers.

Who Is Exempt from Filing Form 941?

The following employers are usually exempt from completing Form 941:

- Seasonal employers that do not pay wages or have no payroll tax liability during a quarter are permitted to skip the filing obligation for that quarter.

- Small employers, if their annual payroll tax liability is $1,000 or less, are directed by the IRS to file Form 944 instead.

- Employers with an agricultural occupation whose employment taxes are reported via Form 943 instead of Form 941.

- Household employers (employers who employ nannies or caregivers) that file taxes using Schedule H with their individual return.

- Employers with no employees and that have no wage tax liability for the whole quarter.

Differences Between Form 940 and Form 941

| Factors | Form 940 | Form 941 |

| Taxes reported | Federal unemployment tax | Income tax withheld, Medicare, and Social Security Tax |

| Filing frequency | Annual (Due Jan 31/Feb 2, 2026) | Quarterly (Apr 30, Jul 31, Oct 31,Jan 31) |

| Wage base | First $7,000 per employee | Varies |

| Who pays? | Employer only | Employer + employee shares |

| Threshold to file | $1,500 wages | Wages subject to withholding / Medicare |

Instructions To Fill Form 940

Following the proper instructions for Form 940 is critical to avoid IRS penalties.

Here’s a section-by-section guide:

- Top Section- Identifying Information: Enter your Employer Identification Number (EIN) exactly as it appears in IRS records. Never use a Social Security Number on a form requesting an EIN.

- Part 1 State Unemployment Tax: Line 1a asks for the state abbreviation if you paid state unemployment taxes in only one state. Line 1b requires checking a box if you operated in multiple states and then completing Schedule A. Line 2 requires noting if you paid wages in a credit reduction state.

- Part 2 FUTA Tax Before Adjustments: Line 3 enters your total payments to employees. Line 4 exempts payments such as retirement plan contributions and fringe benefits. Line 5 calculates taxable FUTA wages (subtract exempt amounts). Line 6 computes the gross FUTA tax at 6%.

- Part 3 Adjustments: This is where you apply your state unemployment tax credit (up to 5.4%), reducing your effective FUTA tax.

- Part 4 FUTA Tax and Balance Due: Enter any deposits made throughout the year and calculate the balance owed or overpayment.

- Part 5 Report Your FUTA Tax Liability by Quarter: Complete this section only if your total FUTA tax for the year exceeds $500.

- Signature: An unsigned Form 940 is considered invalid by the IRS. If filing electronically, use your IRS-authorized e-file signature PIN.

Where to Mail Form 940?

If you choose to file by paper rather than electronically, where you mail Form 940 depends on your state and whether you’re including a payment. The IRS mailing address for Form 940 changes periodically, so always verify the correct address against the current year’s IRS Form 940 instructions before mailing.

As a general rule:

- Employers in certain states use one IRS processing center address.

- Employers in other states use a different address.

- When including a payment, the address often differs from the address used without a payment.

Best practice: E-file through the IRS Modernized e-File system or IRS-approved software. Not only is it faster, but if your tax preparer files more than 10 returns during the 2025 filing season, e-filing is required by law.

Common Mistakes to Avoid When Filing Forms 940 and 941

Here we mentioned some of the common mistakes most of the people make while filing form 940 and 941.

- Misclassifying Workers: Calling an employee an independent contractor eliminates your obligation to file Form 941 for that worker, but if the IRS disagrees with your classification, you face back taxes, penalties, and interest. When uncertain, file IRS Form SS-8 to get a formal determination before a costly audit forces the issue.

- Missing Deadlines: The IRS charges separate penalties for failure to file and failure to pay. Both can accumulate quickly, especially for quarterly Form 941 filers.

- Incorrect EIN: A single transposed digit in your Employer Identification Number can cause rejected returns, delayed processing, and IRS notices. Double-check your EIN against your IRS assignment letter every time you file.

- Failing to Deposit FUTA Taxes Quarterly: Many employers forget that while Form 940 is filed annually, FUTA tax deposits are required quarterly whenever the cumulative liability exceeds $500. Missing these deposits triggers deposit penalties on top of the annual filing requirements.

Should I File Both Form 940 and 941?

In almost all cases, yes, if you have employees, you likely need to file both forms.

- Form 940 handles FUTA.

- Form 941 handles income tax withholding and FICA.

They cover entirely different tax obligations under different sections of federal law. Skipping one because you’ve filed the other is a compliance error with real penalties.

The only scenario where you might file Form 940 without Form 941 is if your payroll taxes are so minimal that the IRS has authorized you to file Form 944 annually instead. Even then, Form 940 still has its own annual filing requirement. To stay organized year-round, many employers review paystubs made with the proper paystub template formats to maintain consistent payroll records that support both quarterly and annual tax reporting.

Key Takeaways

The form 940 vs 941 comparison ultimately comes down to this: annual vs quarterly, unemployment vs payroll taxes, employer-only vs shared employee-employer responsibility. Once you internalize these three distinctions, the rest of the rules, deadlines, deposit schedules, and credit reductions fall into a logical place.

People May Also Ask

1) What is the difference between 940 and 941?

Form 940 is used to report FUTA taxes; however, Form 941 is used to report federal income tax withheld, Social Security, and Medicare taxes witholding.

2) Is FUTA the same as 940?

FUTA is the tax law, while Form 940 is the form used to report it.

3) What is the meaning of 941?

Form 941 is a type of quarterly tax form filed by employers to report their payroll taxes to the IRS.

4) What is a Schedule B for 941?

File Schedule B (Form 941) if you are a semiweekly schedule depositor. You are a semiweekly depositor if you: Reported more than $50,000 of employment taxes in the lookback period. A tax liability of $100,000 or more has accrued on any day in the current or prior calendar year.

5) What are Forms 940 and 941?

Form 940 is used to report FUTA taxes, while Form 941 is used to report federal income taxes withheld, Social Security, and Medicare taxes withheld.

Also Read:

What is Gross Pay? And How To Calculate It?

How To Get a Walmart W2 Former Employee Form In 2026?

W9 vs W4: How These Tax Forms Differ and Why They Matter