If you’re a small business owner who is eager to save taxes with Form 8995, then you have landed on the right page. The IRS introduced this form as part of the Qualified Business Income (QBI) deduction, which allows eligible taxpayers to deduct up to 20% of their business income.

In this guide, we will be covering everything you need to know about Form 8995, including its purpose, who is eligible, and how it differs from the similar and more complex Form 8995.

Accurate check stubs are the backbone of smooth payroll processing and financial transparency. Instead of dealing with complex calculations, switch to a smarter solution. Use the pay stub generator and create detailed, compliant check stubs in just a few clicks.

What is Form 8995?

Form 8995 is the simplified tax form that is used to calculate and claim the Qualified Business Income (QBI) deduction. The QBI deduction allows you to deduct up to:

- 20% of qualified business income

- Plus 20% of REIT dividends and PTP income

This deduction is applied to the following:

- Sole proprietors

- Partnerships

- LLCs

If you own a pass-through business that has earned $150,000 in qualified income as a sole proprietor, the QBI deduction will allow you to reduce your taxable income by 20% of your taxable income for that year is $120,000.

What is Form 8995 a?

Form 8995-A is the advanced QBI deduction form. The IRS says that when taxable income is before the QBI deduction is above $197,300 for most of the filers, or when the taxpayer is a patron of an agricultural cooperative.

The form uses separate schedules: Schedule A, Schedule B, Schedule C, and Schedule D. This is the form that applies when the deduction gets more technical. It handles wage limits and specified service trade, aggregation, and cooperative-related calculations.

Why is the 8995 Form important?

The IRS Form 8995 plays a vital role in reducing taxable income for millions of businesses.

Major Benefits:

- It reduces your taxable income notably

- Simplifies complex tax calculations

- Saves time as compared to Form 8995 a

- Helps in maximizing Section 199A deductions

If used correctly, this form can save thousands in taxes annually.

What is Qualified Business Income (QBI)?

Qualified Business Income (QBI) is defined as the net amount of qualified items of gains, deductions, and losses from a qualified business that operates in the U.S. This includes income flowing to your personal return through Schedule C, Schedule F, or Schedule K-1 from a partnership, S corporation, or trust.

What is not included in the QBI?

The Form 8995 instructions are explicit about items that must be excluded from your QBI calculation:

- Capital gains and losses

- Dividends

- Interest income not properly allocable to a trade or business

- Reasonable compensation paid to yourself by an S corporation

- Guaranteed payments from a partnership

- Section 707(a) payments for services rendered to a partnership

- Commodities transactions and foreign currency gains or losses

- Income from outside the United States

- Wages received as a W-2 employee

Step-by-Step Guide to Filling Out Tax Form 8995

Understanding Form 8995 is important for accurate tax filings. Below, we have shown a breakdown of a step-by-step guide for filing out the tax form:

Insert Qualified Business Income

List down each business and its QBI:

- Combine profits and losses

- Carry forward the previous losses

Multiply by 20%

Calculate it: QBI × 20%

Add REIT & PTP Income

Include: REIT dividends and publicly traded partnership income, and multiply it by 20% again

Apply Income Limitation

Your deduction is the lesser of:

- 20% of QBI

- 20% of taxable income

Final Deduction

Insert the final number on your Form 8995

Example of Form 8995

Let’s say you are a single filer and have Qualified business income: $120,000

Filing status: Single Income below the IRS threshold

Usually, the tax deduction is 20% of QBI, so: $120,000 20% = $24,000

Based on this, your QBI deduction will lower your taxable income by $24 000, but keep in mind that it is in accordance with the rules of the form and any other deductions/limitations that may apply. The IRS instructions for Form 8995 explain that the form is the simplified version of the calculation for this type of deduction.

What are Form 8995 instructions?

The following are the Form 8995 instructions:

Determine Qualification

Check if you qualify for the QBI deduction, which is generally available to individuals, estates, and trusts with income from pass-through entities such as sole proprietorships, partnerships, LLCs, and S corporations, provided their taxable income is below certain limits.

Calculate QBI

Your QBI consists of Internet earnings outside of your pass-through enterprise; however, capital gains, hobby income unrelated to the enterprise, salary gains, and foreign gains are excluded.

Download Form 8995

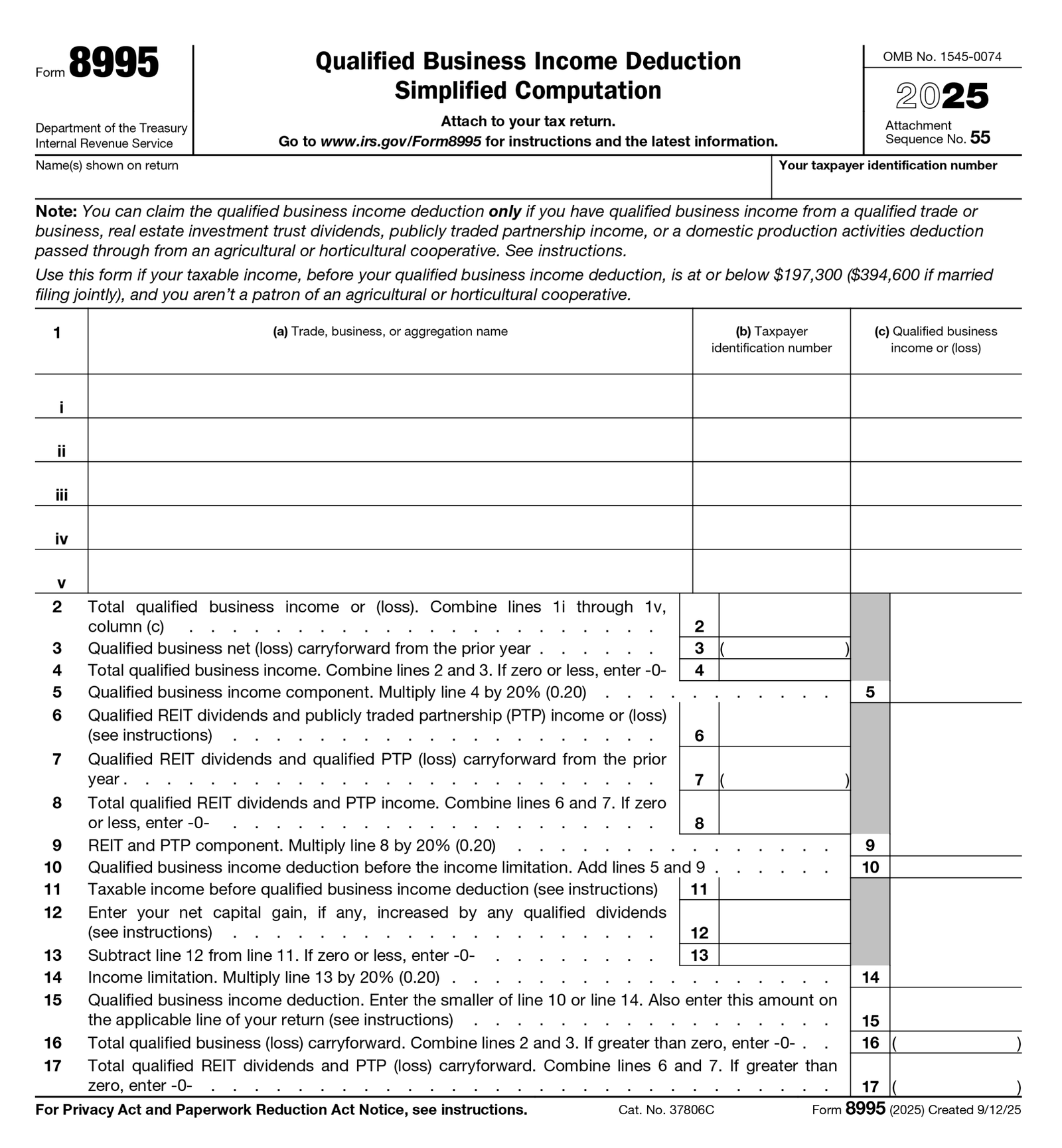

Get the official IRS Form 8995 PDF from the IRS website.

Fill in the Form details

Lines 1-4: Enter your business information and calculate your total QBI.

Lines 6-10: Report income from Real Estate Investment Trusts (REIT) or Publicly Traded Partnerships (PTP) if applicable.

Lines 11-15: Calculate the QBI deduction, considering your total taxable income and net capital gains.

Lines 16-17: Determine any carryover loss, which can be used to offset future profits if your net QBI is negative.

Loss carryforward

If you have a loss in business, it can be carried forward to reimburse QBI in future years. Loss from one commercial enterprise can offset QBI from different companies even if you own a lot in a couple of entities.

Review & submit

Attach Form 8995 to your tax return and make sure all information is accurate before filing with the IRS.

Who needs to file the 8995 Form?

Understanding what Form 8995 is means first understanding who it applies to. You should use Form 8995 (the simplified version) if all three of the following conditions are true:

- You have QBI, qualified REIT dividends, or qualified publicly traded partnership (PTP) income or loss.

- Your 2025 taxable income before the QBI deduction is at or below $394,600 (married filing jointly) or $197,300 (all other filing statuses).

- You are not a patron of a specified agricultural or horticultural cooperative.

Form 8995 vs Form 8995-A: Key Differences [Table]

| Factors | Form 8995 | Form 8995-A |

| Purpose | Simplified QBI deduction | Advanced QBI deduction |

| Income Level | At or below the threshold | Above the IRS threshold |

| 2026 Threshold | Income below $197,300 / $394,600 | Income above threshold |

| Schedules Required | No separate schedules | Schedules A, B, C, and D |

| Best For | Easy pass-through income | More complex filers |

When Should You Use Form 8995-A Instead?

You should use Form 8995-A when:

- Your taxable income exceeds IRS limits

- You have a complex business situation

- You’re in a Specified Service Trade or Business and above the threshold

- You must apply W-2 wages or UBIA property limits

- You have REIT dividends or PTP income

What makes 8995 A more complex?

The twist of 8995 Form A comes from the extra rules that are built into the QBI deduction. IRS instructions require separate schedules for:

- Schedule A for specified service trades

- Schedule B for the aggregation of business operations

- Schedule C for loss netting and carry-forward

- Schedule D for special rules for patrons of agricultural cooperatives

Common Mistakes When Filing Form 8995

There are a few mistakes to watch out for while filing out Form 8995:

- Using the wrong form for the earning level

- Forgot to include the REIT dividends where applicable

- Misclassifying SSTB

- Skipping the required schedule on Form 899-A

- Reporting the wrong qualified business income amount

- Not carrying forward prior-year losses correctly

Key Takeaways

The decision to use either Form 8995 or Form 8995-A depends on your taxable income, business type, and whether you are subject to any particular QBI provisions. Generally, if you have a simple tax return and your income is under the IRS limit, Form 8995 is the appropriate one. However, if your income is high or your filing situation includes SSTBs, a combination of businesses, wage limitations, or rules for cooperatives, then Form 8995-A is the one you should look at.

Curious Mind Also Ask

1) What Is Form 8995?

Form 8995 is a simplified IRS tax form used by eligible businesses to calculate and claim the Qualified Business Income deduction.

2) Is there a penalty for not filing Form 8995?

Failure to file Form 8995 penalty is 5% of the unpaid taxes for each month the return is filed late, up to a maximum of 25%.

3) Why do I have Form 8995 in my tax return?

Form 8995 is included in your tax return to calculate the Qualified Business Income (QBI) deduction. This deduction allows eligible taxpayers to deduct up to 20% of their qualified business income from a pass-through entity, such as a sole proprietorship.

4) How do I know if my business qualifies for QBI?

Your business generally qualifies for the Qualified Business Income (QBI) deduction if you operate as a sole proprietorship, partnership, S corp, or LLC, and have net income.

5) Why do I have QBI on my tax return?

You have a Qualified Business Income (QBI) deduction (Section 199A) because you earned income from a pass-through business, such as a sole proprietorship, partnership, or S corporation.

6) Is an LLC eligible for QBI?

Yes, an LLC can qualify for the Qualified Business Income (QBI) deduction (Section 199A). LLCs are pass-through entities, allowing members to deduct up to 20% of their share of qualified business income from their personal tax returns, provided the business meets specific requirements, including being US-based.

Also check:

Create a W2 Form Online Instantly!

FAQ's

What is 8995 qualified business income deduction?

+

IRS Form 8995 (Qualified Business Income Deduction Simplified Computation) is used by eligible sole proprietors, partners, S corp shareholders, and beneficiaries to calculate their $20% pass-through tax deduction.

Why am I not getting a QBI deduction?

+

If the QBI info is not recorded in the codes, the IRS will assume it is not a qualifying business, so the taxpayer will not be allowed to take the deduction from the pass-through entity.

Who must file the IRS Form 8995?

+

Form 8995 is the IRS tax form that owners of skip-through entities, sole proprietorships, LLCs, or S corporations use to take a qualified business income (QBI) deduction, also called a bypass-through or Section 199A deduction.

Where to report Form 8995?

+

The Form 8995 used to calculate the QBI deduction of the S component needs to be attached as a PDF to the ESBT tax worksheet filed with Form 1041. When attached to the ESBT tax worksheet, the trust must show that the records are best applicable to the S element.