Lenders require additional information when reviewing your application for personalized loans. They meticulously examine your financial documents to confirm your income, employment, and capacity to repay the loan. A borrower often uses a free paystub generator in order to create a professional income record and maintain payroll documents. The well-prepared documentation not only expedites the success but also aids in avoiding delay periods as much as possible.

Whether you are applying for just a loan online or at a bank, knowing which documents will be needed enhances your ability to receive an approval at a better personalized rate.

You typically need a government-issued ID, pay stubs, proof of income, bank statements, employment verification, proof of address, and a completed loan application to apply for personalized loans.

In this guide, we will walk you through some of the necessary documents that could be required when applying for traditional loans / customized loans, like proof of income, employment verification, bank statements & pay stubs.

What is a Personal Loan?

A personal or personalized loan is a type of financing that allows a person to borrow a fixed amount of money from a bank, credit union, or online lender and repay it over time through timely automatic payments.

A personal loan is a kind of credit in which you obtain a fixed amount from a financial partner or just a lender and repay it in monthly installments. This type of loan is typically used for several expenses, such as medical bills, personal loans debt consolidation, home repairs, or emergency costs due to illness, weddings, and other major purchases.

Since most personal loans in the market today are unsecured, you do not need to put up anything of value (like your house, car or other assets) as collateral to qualify. Instead, you need to provide a flat personal loan rate of interest based on your credit score, lenders’ details like your income, credit history, employment status, and debt-to-income ratio before giving you a loan. That said, preparing documents like check stubs, bank statements, and proof of employment can increase your odds of being approved.

What Documents Do You Need for a Personal Loan?

When applying for personalized loans, lenders will request various loan documents in order to confirm your identity and income source, along with your employment status and overall financial health. By preparing these documents beforehand, you can potentially accelerate the approval process and minimize delay and prepayment penalty.

Requirements depend on the lender, but generally speaking, your personal loan application will seek to proof of identity, proof of your income, verification of employment, and address, as well as details regarding your finances.

1. Proof of Identity

Before lenders approve a loan application, they need to verify who you are. A government-issued photo ID is always required as proof of your identity.

Commonly accepted IDs include:

- State-issued ID card

- Social Security card

- Passport

- Driver’s license

- Birth Certificate

Certain lenders may ask you for more than one ID to protect against fraud and identity theft. Often, this is simply submitting a valid photo ID and Social Security number.

Some lenders may request multiple identification documents to prevent fraud and identity theft. In most cases, a valid photo ID and Social Security number are enough to complete this step.

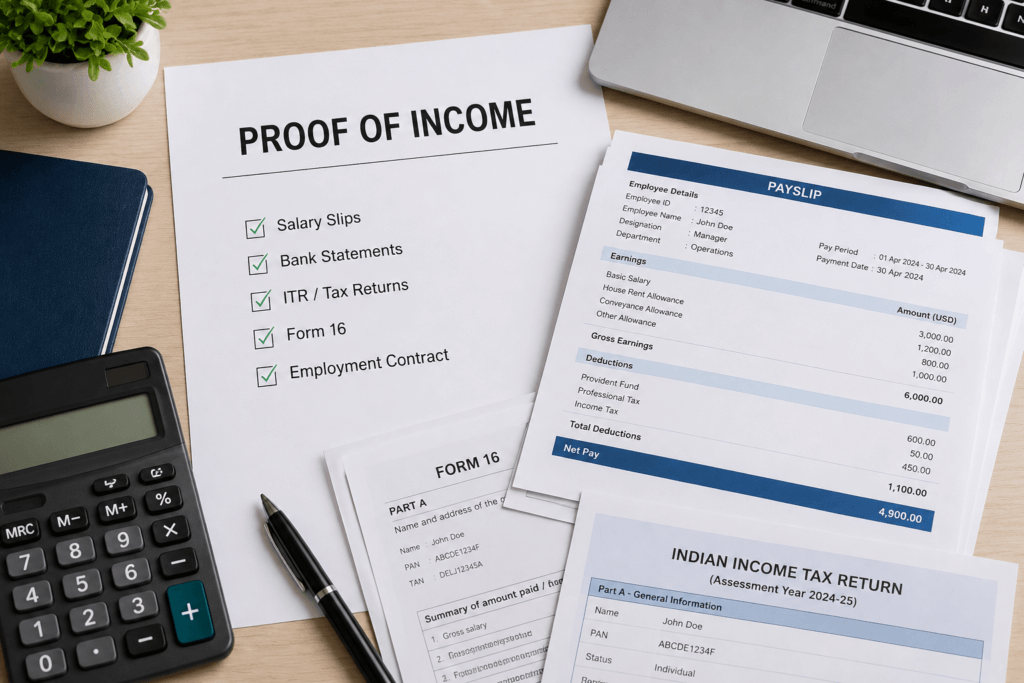

2. Proof of Income

Proof of income allows you to show lenders that you can afford to repay the personal loan without straining your finances. It also helps them determine the potential amount of money you can borrow.

If You’re a W-2 Employee:

You may need to provide:

- Recent pay stubs from the last 1-2 months

- W-2 forms from the past 1–2 years

- Employer contact information

Most of the time, borrowers go for a paystub creator to create pay stubs in a systematic way, which expedites the income verification process necessary to approve their loan application.

If You’re Self-Employed:

Self-employed applicants are often required to provide additional personal loans pre approval financial documents, such as:

- Tax returns from the past two years

- Bank statements showing regular income deposits

- Profit and loss statements

- 1099 forms

Because self-employed income can fluctuate from month to month, detailed self employed proof of income records help demonstrate stability and repayment ability.

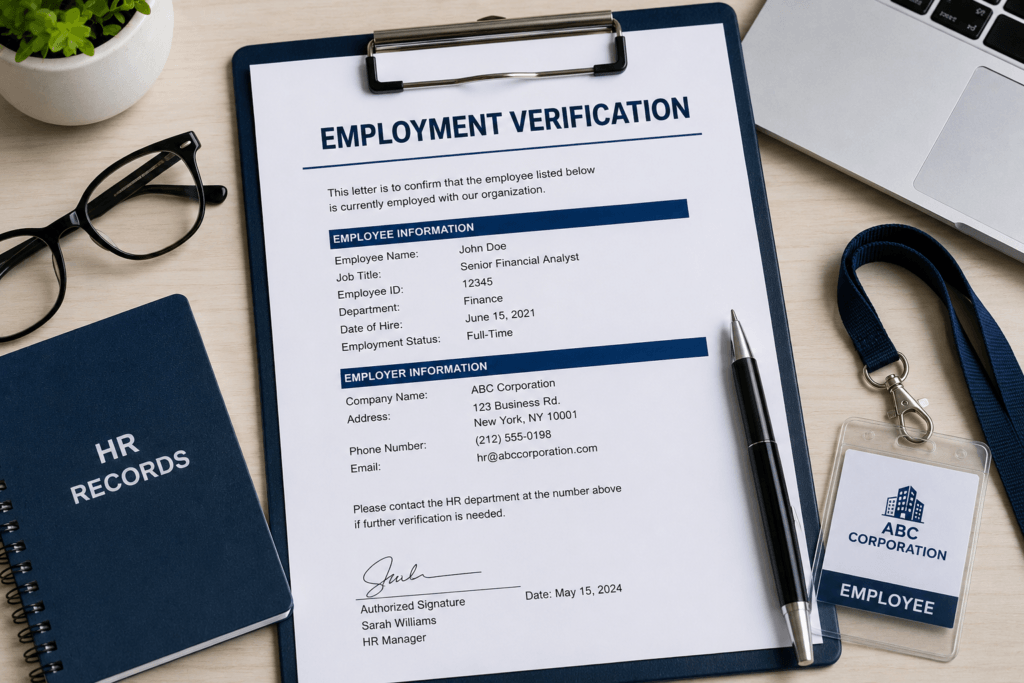

3. Employment Verification

Lenders also verify your current employment status to confirm you have ongoing income.

Employment verification may include:

- Employer contact details

- A recent pay stub

- A signed employment verification letter

- Employment contract or offer letter

Retired applicants may provide pension statements instead.

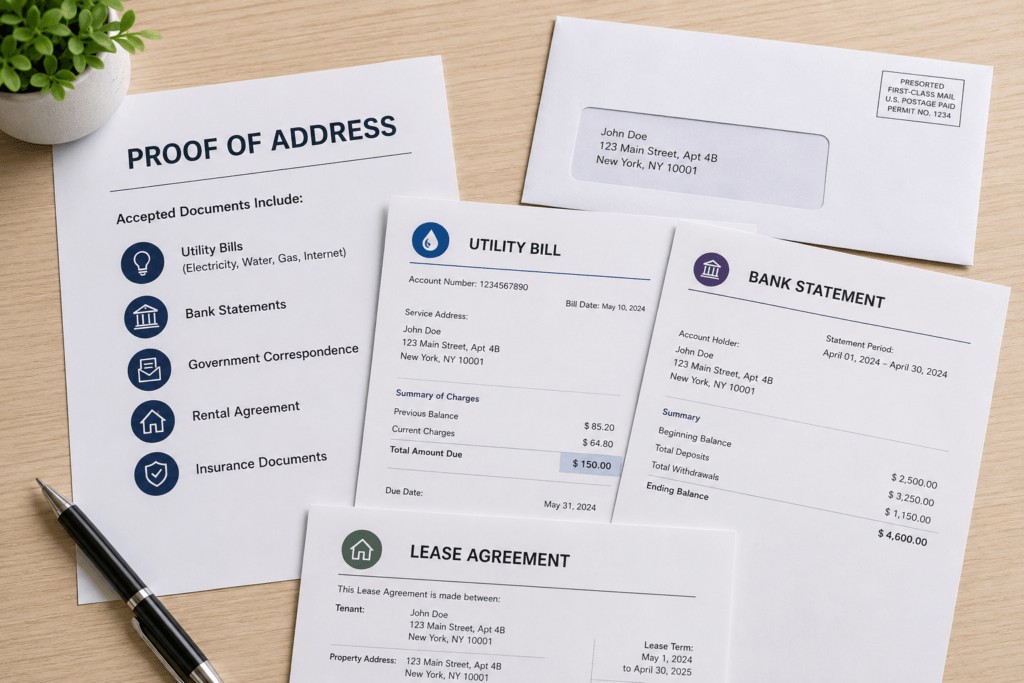

4. Proof of Address

This is usually needed, as most lenders will ask to see proof of where you live.

Accepted documents may include:

- Lease or rental agreements

- Utility bills

- Voter registration cards

- Mortgage statements

- Bank statements with your address

Your identification papers must usually tie up with all of your help documentation at the same address.

5. Credit History Authorization

Most lenders check your credit before granting personalized loans.

Rather than bringing your own credit report, most often you will provide written or digital consent for the lender to access yours.

This allows lenders to review:

- Existing debts

- Your credit score

- Payment history

- Recent credit inquiries

Reviewing your credit report prior to applying will allow you to identify and remedy any errors.

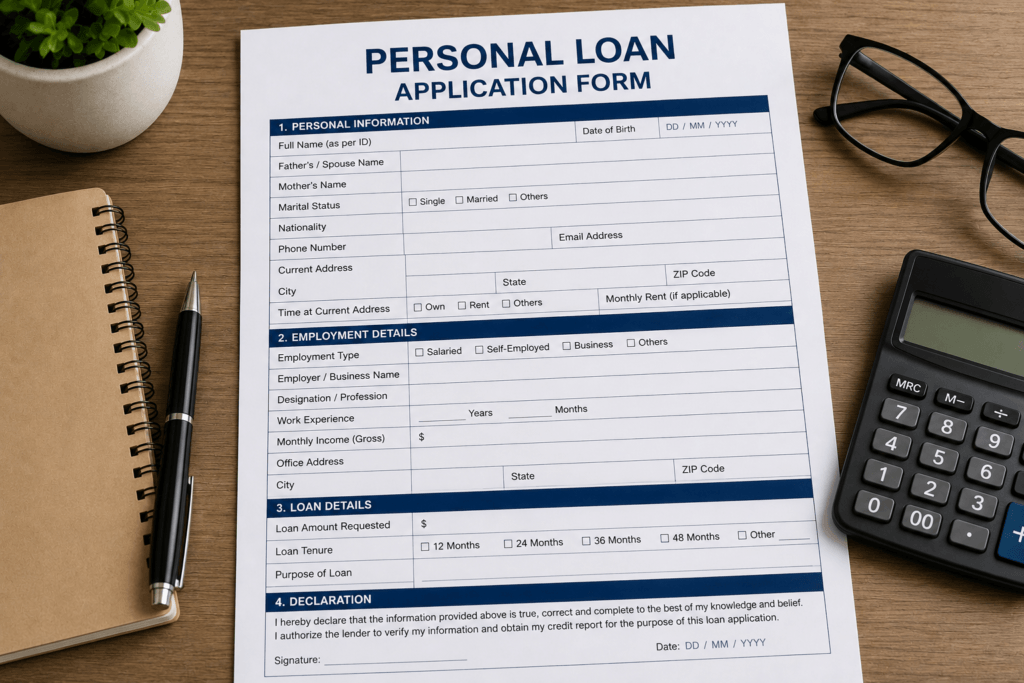

6. Personal Loan Application Form

All lenders need a filled-out loan application.

The personal Loan US bank application includes personal and financial information like:

- Social Security number

- Full name and date of birth

- Employment and income details

- Contact information

- Intended loan purpose

- Debt obligations

- Requested loan amount

As delays can take place when the details differ, maintaining consistency and accuracy in information is necessarily important.

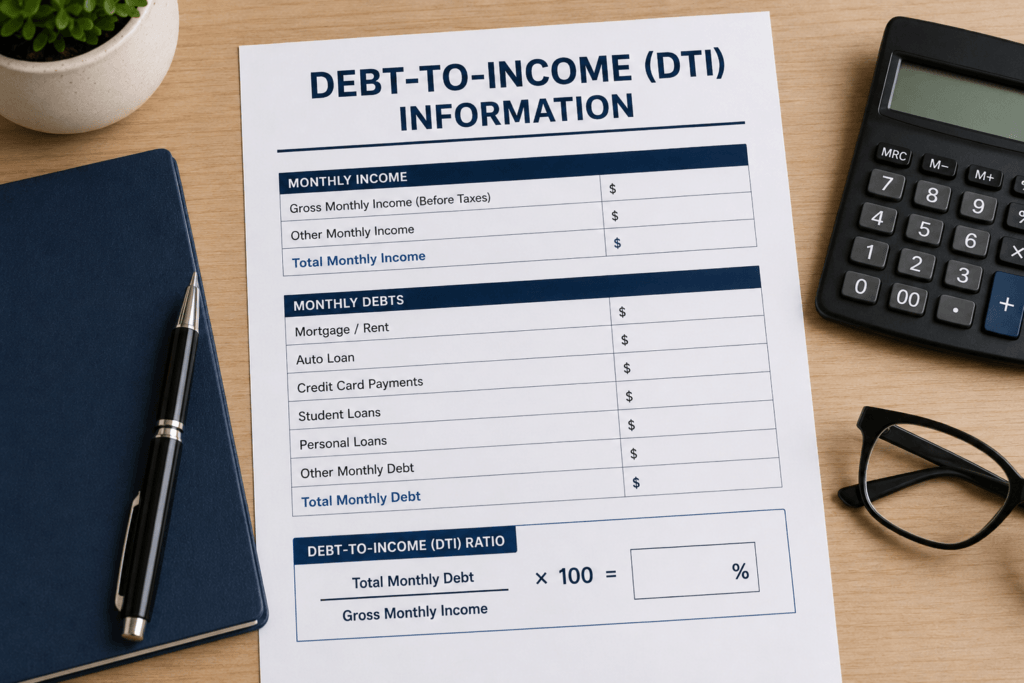

7. Debt-to-Income (DTI) Information

Your debt-to-income ratio helps lenders understand how much of your income already goes toward debt payments.

If your DTI ratio is high, lenders may request additional documents, such as:

- Credit card payment details

- Rent or mortgage payments

- Car loan statements

- Child support or alimony obligations

- Co-signed loan agreements

A lower DTI ratio generally improves your chances of loan approval.

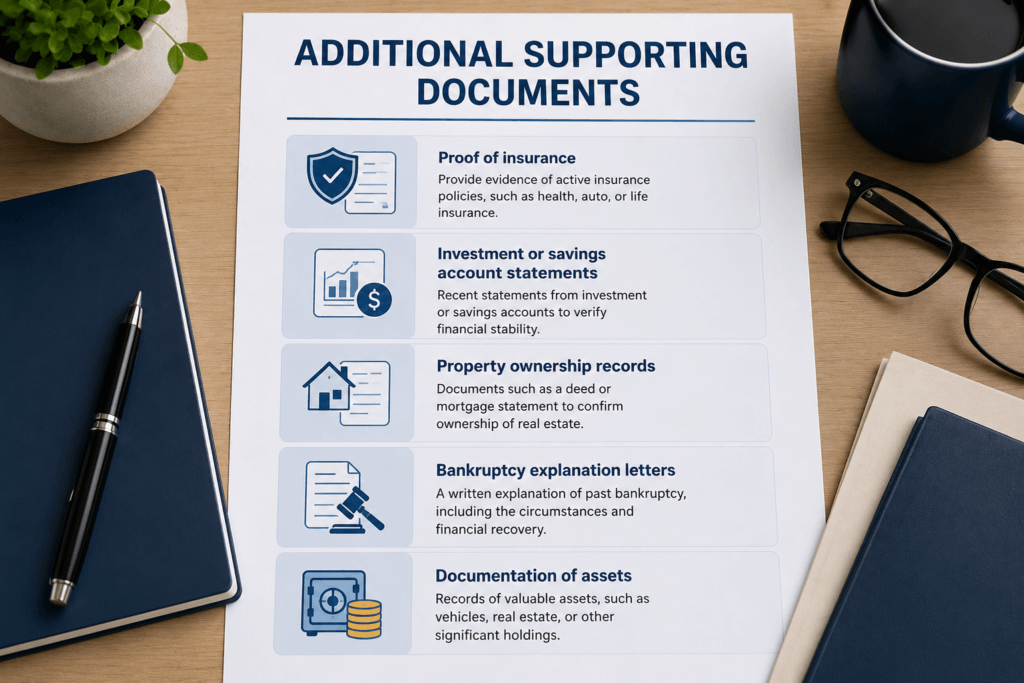

8. Additional Supporting Documents

Your credit profile and lender guidelines will play a role.

You may also need to provide extra documentation, including:

- Proof of insurance

- Investment or savings account statements

- Property ownership records

- Bankruptcy explanation letters

- Documentation of assets

Digital documents uploaded online can be reviewed for faster approvals with lenders, while traditional banks and credit unions typically involve more paper documentation and manual verification.

Getting all your papers in order prior to applying will allow for a quicker, smoother, and more likely chance of getting approved while taking an individualized loan approach.

Eligibility Criteria For Guaranteed Personalized Loans

Before applying for guaranteed personalized loans, it’s important to understand the basic eligibility requirements lenders use to evaluate borrowers. Although every lender follows different approval guidelines, most consider factors such as credit score, income stability, debt-to-income ratio, and financial history before approving a loan application.

Here’s a breakdown of the most common requirements for personalized loan approval.

1. Credit Score and Credit History

Your credit score is one of the most important factors lenders review when deciding whether to approve your loan application. A strong credit score shows responsible borrowing habits and increases your chances of receiving personal loans best interest rates and flexible repayment terms.

2. Stable Income and Employment Verification

Lenders need proof that you can comfortably repay the loan. That’s why they usually require documents that verify your income and employment status.

3. Debt-to-Income (DTI) Ratio

Your debt-to-income ratio measures how much of your monthly income goes toward paying existing debts. Lenders use this ratio to determine whether you can manage additional loan payments responsibly.

4. Collateral Requirements

Most personalized loans are unsecured, meaning you do not need to provide collateral such as a car or home. Unsecured loans generally offer faster approvals because lenders do not need to evaluate assets.

However, some lenders also offer secured personal loans for borrowers who may not qualify otherwise.

How to Qualify for Personalized Loans?

Every lender has different requirements when it comes to loan approval, so there are a few valuable steps you can take before submitting your application to enhance the odds that you land the loan terms and interest rates.

Improve Your Credit Score

Your chance of securing personalized loans is heavily impacted by your credit score. A 670 or higher credit score is generally considered a responsible score, which is why Personal Loans Credit Union is okay with it.

Maintain Proof of Stable Income

Lenders typically want to see proof of income before approving personalized loans. Things like bank statements, W-2 forms, tax returns, and pay stubs here help confirm your earnings and employment verification.

Lower Your Debt-to-Income (DTI) Ratio

Lenders will assess your debt-to-income ratio since they want to ensure you can easily take on an additional monthly payment. A high DTI ratio can lead lenders to see you as financially stressed, making them not want to give you approval.

Apply With a Cosigner

If your credit history is shorter or you have a lower score, this can help to add a cosigner to your application. A cosigner with good credit and steady income minimizes the lender’s risk, which could lead to lower rates.

Consider Secured Loan Options

Many lenders provide secured personal loans, which need some form of collateral (similar to a vehicle, savings account, or investment accounts). Because they reduce the risk to lenders, secured loans generally have lower interest rates.

What to Do If Your Personal Loan Application Gets Rejected?

If you are not eligible for a traditional personal loan USA, there are many other paths to consider to handle your financial situation:

- Seek temporary financial assistance from trusted friends or family

- Create your own paystub by considering the preferred paystub template

- Explore secured loan options using assets

- Request flexible repayment arrangements

- Check personalized loans reviews to avoid future hurdles

- Sell unused household belongings, electronics, furnishings, or clothes

How Do I Apply for Personalized Loans?

Getting a personal loan helps greatly if you prepare your financial documents beforehand. With online applications and fast approvals, lenders are able to provide a speedy experience for potential borrowers. Knowing each step can save you time and increase your chances of doing it right the first time.

- Understand Your Financial Needs: Before applying for the loan, identify why you need that kind of money and find out how much you really want to take.

- Check Your Credit Score: Check your credit score and report to know how I get loan, how good or bad the standing of your finances is, and what is personalized loans difference.

- Compare Different Lenders: Look into local banks and credit unions to find the best interest rates and learn about the personal loan criteria lenders require for approval, such as a certain income or credit score.

- Complete the Loan Application: Provide your application, supporting documents like income verification, ID verification, or bank statements

- Review and Accept the Loan Offer: Once you have an offer, review the details such as loan terms and repayment schedule, loan fees or origination charges, and monthly payments.

Final Thoughts

When you have all the documents ready, applying for personalized loans is much easier. Arranging documents ahead of time can significantly reduce delays, expedite the benefit approval process, and increase approval rates. Before issuing you a personal loan, lenders want to see definitive proof of your identity, income status, employment status, and financial stability.

Be it a salaried, freelancer, self-employed professional, or gigworker, you need to maintain income records. Several people use pay stub generator to produce neatly organized pay stubs that are designed for easy reading during the income verification process.

If the preparation work is done and proper documentation is ready, you will be in a better position to get the right loan for debt consolidation, handling any emergency expenses, major purchases, or other goals.

People May Ask

1. What is the easiest loan to get approved for?

Secured loans with fair or bad credit are usually the easiest to get approved for because they have more flexible criteria.

2. How to get a personalized loan?

To get a personalized loan, you need to compare personalized loan lenders, check your credit score, submit an application, and provide documents.

3. Is getting a personal loan a good idea for debt consolidation?

Yes, a personal loan is a good option because it combines multiple debts into monthly payment with a lower interest rate.

4. Does debt consolidation hurt your score?

Debt consolidation may temporarily lower your credit score, but consistent payments can improve your score over time.

5. Is it better to get a personal loan through a credit union?

Credit unions often offer flexible repayment terms, lower interest rates, and more personalized service compared to traditional banks.

6. Does U.S. Bank give out personal loans?

Yes, the U.S. Bank offers personal loans with fixed rates and flexible repayment options.

7. Who gives the best interest rate on a personal loan?

The best interest rates are usually offered to people with stable income, excellent credit scores, and low debt-to-income ratios.

8. Which bank is the lowest interest rate for a personal loan?

The lowest personal loan rates are typically offered through credit unions and certain online lenders, based on your credit profile.

9. What are the criteria for a personal loan?

A personal loan approval process typically focuses on factors such as your credit score, income level, employment stability, debt-to-income ratio, and how well you have paid back previous loans.

10. Is personalized loan safe?

Yes, generally, personalized loans are safe provided you borrow from a licensed and reliable lender and read the fine print of the loan terms before accepting.

FAQ's