If you’re a small business owner, freelancer, or self-employed individual, understanding the QBI deduction can reduce your tax burden remarkably. Enacted under the Tax Cuts and Jobs Act (TCJA), the Qualified Business Enterprise Gain Deduction, also known as Section 199A, allows eligible taxpayers to deduct up to 20% of their qualified business earnings. Using a reliable pay stub generator can also help you maintain accurate income records, which is essential when calculating your QBI deduction.

In this blog, we will be talking about the QBI deduction, who qualifies, how it works in 2025 and 2026, and how to maximize your business income deduction while staying compliant.

What is Qualified Business Income (QBI)?

Qualified Business Income- QBI is the net amount of qualified items of income, deduction, gain, and loss from any qualified trade or business.

This includes income from partnerships, S corporations, and sole proprietorships.

The QBI amount is reduced by the deductible part of self-employment income and deductions for contributions to qualified retirement plans. But not all business-related expenses do include:

- Capital gains or losses

- W-2 wages earned as an employee

- Dividends and investment interest income, which is not allocable to trade or business

- Guaranteed payments to partners for services

What is Qualified Business Income Deduction?

The Qualified Business Income (QBI) Deduction, also known as the Section 199A deduction, is a tax break that allows eligible business owners to deduct up to 20% of their qualified business income from their taxable income.

Why Does the QBI Deduction Matter?

The QBI deduction matters because of the following reasons:

- Reduces when taxable income exceeds by 20%

- Applies to multiple business structures

- It encourages entrepreneurship

- It can be combined with other deductions

Who Qualifies for the QBI Deduction?

In order to qualify for the qualified business income, you must meet the following criteria:

Eligible Entities

- Sole proprietorship

- Partnerships

- S corporations

Non-Eligible Entities

- C corporations

- Net income

What Counts as a Qualified Business Deduction?

Below are the examples of what counts as a qualified business deduction:

- Net profits from your sole proprietorship

- Deductible self-employment tax

- Self-employed health insurance premiums

- Retirement contributions

- Unreimbursed partnership expenses

- Business interest expenses

What Doesn’t Count as a Qualified Business Deduction?

Below are the examples of what do not count as a qualified business deduction:

- C corporation income

- Wages you pay to yourself

- Investment income

- Interest income that is not related to the business

- Income earned outside the U.S. from foreign businesses

- Rental income

- Guaranteed payments from a partnership

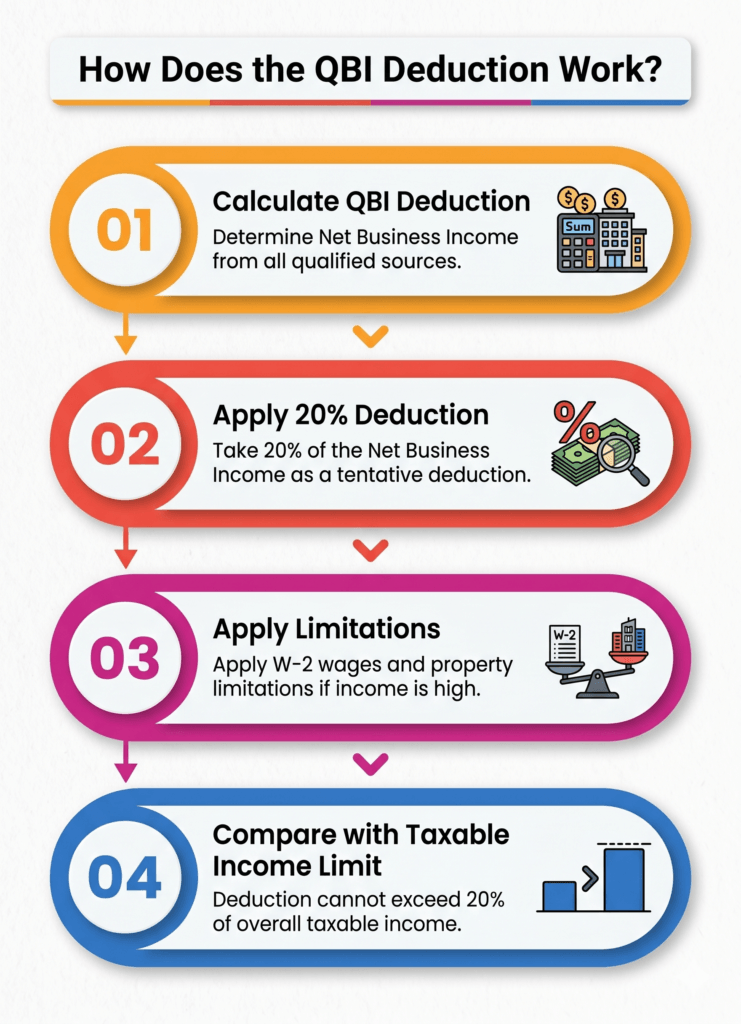

How Does the QBI Deduction Work?

Below is how a QBI deduction works:

1. Calculate QBI Deduction

Determine your qualified business income from each business

2. Apply 20% Deduction

Multiply QBI by 20%

3. Apply Limitations

W-2 wages paid, UBIA of qualified property, SSTB restriction

4. Compare with Taxable Income Limit

The deduction cannot exceed 20% of your total taxable income

What is the UBIA of Qualified Property?

The Unadjusted Basis Immediately After Acquisition (UBIA) is defined as how much of your qualified business property, which might help preserve your deduction once certain income thresholds are met. It measures the value of the depreciable assets you invested in, based on the property’s cost when it was first acquired in service for your business.

UBIA is not reduced by:

- Depreciation taken over time

- Section 179, 179B, or 179C expensing

- Basis adjustments for investment

UBIA is reduced when:

- The property is not used in the specified service trade or business during the year

- A portion of the asset is used for personal business purposes

Why UBIA Matters in QBI Deduction

UBIA is used when your income is above the QBI threshold.

It helps determine how much deduction you can still claim if:

- Your business is subject to W-2 wage and property-based limitations

- You exceed income limits

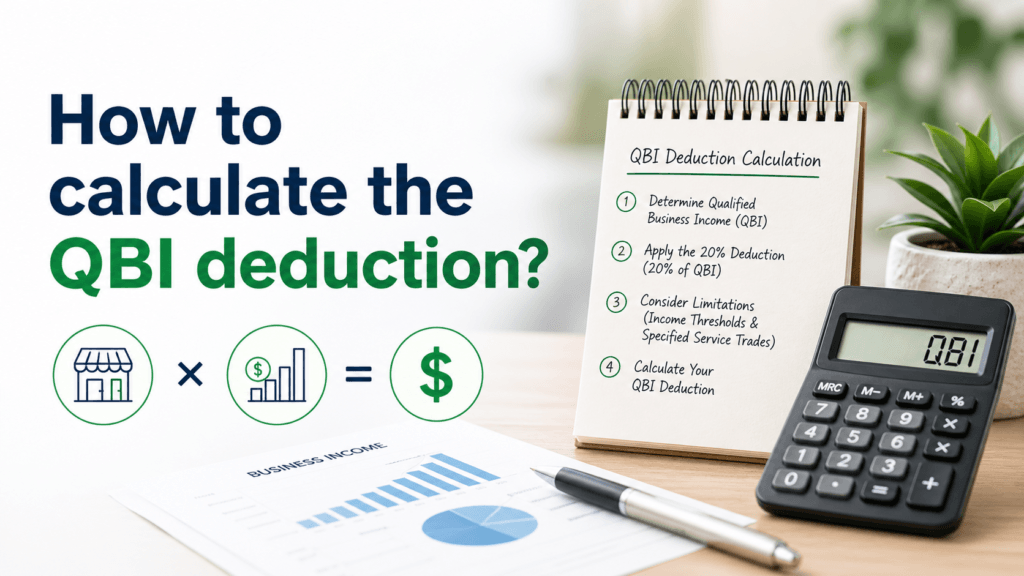

How to Calculate the QBI Deduction?

Calculating the Qualified Business Income Deduction, due to its complexity, the tax preparer will need a lot of technical qbi deduction rules and record-keeping on behalf of the taxpayer. The QBI deduction is calculated by way of using either Form 8995 or 8995A. The form you use to calculate the QBI deduction really depends on the taxpayer’s taxable income (not including the QBID). The deduction begins to phase in at a certain point, and it phases out completely by the top of the threshold.

In some cases, for taxpayers with income at or above the taxable income limits, the calculation is even more complex and may be constrained by further limitations. These taxpayers will need to use Form 8995-A for their QBID calculation. Exceptions exist, for example, for a taxpayer with income below the limits, such as when income is received from a specified agricultural or horticultural cooperative.

How Do You Calculate the QBI Component?

How you calculate your OBI component initially depends on whether your taxable income falls above, below, or within a “phase-in range.” The QBI phase-in ranges for the 2025 and 2026 tax years are shown in the following table.

| Filing Status | 2025 QBI Phase-In Range | 2026 QBI Phase-In Range |

| Married Filing Jointly | $394,601 to $494,600 | $403,501 to $553,500 |

| Married Filing Separately | $197,301 to $247,300 | $201,776 to $276,775 |

| All Other Taxpayers | $197,301 to $247,300 | $201,751 to $276,750 |

What is Section 199A?

Section 199a is a tax provision that was introduced by the Tax Cuts and Jobs Act of 2017, which allows eligible taxpayers to deduct up to 20% of their QBI.

What are Section 199A Dividends?

Section 199A Dividends are a special type of dividend that you receive from:

- Real Estate Investment Trusts

- Publicly Traded Partnerships PTP

These qualified REIT dividends are separately eligible for the same 20% deduction under Section 199A.

| Factors | Section 199A | Section 199A Dividends |

| Source | Business Income | Qualified PTP income investments |

| Require business | Yes | No |

| Deduction | Up to 20% of QBI | Up to 20% of Dividends |

| Reported on | Business tax forms | Form 1099-DIV |

SSTB vs Non-SSTBs: Major Differences

Some agencies rely closely on the skills or accreditation of the owners or employees. These are called Specified Service Trades or Businesses (SSTBs).

What is an SSTB?

An SSTB (Specified Service Trade or Business) is a business where income comes mainly from providing services as per specialized skills.

Examples include:

- Health professionals (doctors, dentists, veterinarians)

- Consulting

- Legal services

- Accounting (CPAs, tax professionals)

- Brokerage services (investment managers, trading, dealing in securities)

- Performing arts (actors, entertainers)

- Athletes

What is a Non-SSTB?

A non-SSTB includes businesses that do not depend primarily on personal expertise.

Examples:

- Retail stores

- Manufacturing businesses

- Real estate businesses

- Engineering and architecture (specifically excluded from SSTB rules)

- Restaurants

Note: Using a reliable pay stub template can help you accurately track your income, making it easier to consider income and taxes and claim your QBI deduction.

Key Difference in QBI Deduction

The main difference regarding SSTBs and Non-SSTBs.

| Feature | SSTBs | Non-SSTBs |

| QBI Deduction (Below Threshold) | Get full QBI deduction | Get full QBI deduction |

| High-Income Treatment | May lose deduction entirely | Subject to W-2 wages and UBIA property limits |

| QBI Deduction (Above Threshold) | Deduction phases out completely | Still qualify for deduction |

| Overall Eligibility | Limited at higher income levels | More flexible, even at higher income |

What is The Impact of Accuracy-Related Penalties on QBID?

Before computing the Qualified Business Income Deduction (QBID), tax preparers must determine whether the activity qualifies as a trade or business under Section 199A. Not all income reported on a return qualifies as QBI, even if it appears on a business schedule.

For taxpayers below the income threshold, the QBID is generally the lesser of 20% of qualified business income or 20% of taxable income (excluding net capital gains). However, for taxpayers within or above the phase-out range, additional limitations based on W-2 wages, qualified property, and SSTB status may apply.

Incorrect QBID calculations can result in accuracy-related penalties, typically 20% of the underpaid tax, especially if the error leads to a substantial understatement of income tax.

How to Claim QBI Deduction?

To claim the deduction for qualified business income, follow these steps:

Forms Required

- IRS Form 8995

- IRS Form 8995-A

Filing Tips

- Maintain accurate records

- Separate business and personal income

- Work with a tax professional

Common Mistakes to Avoid while Claiming QBI Deductions

When you’re helping clients determine their eligibility, and claim the QBI deduction, you need to take care regarding these mistakes:

- Understating Income: Determining qualified business income can be challenging, and it’s easy to over- or understate income, particularly for businesses with multiple income streams.

- Business activities that do not qualify: Certain types of groups may have constraints or rules on QBID. Those entities include (and are not limited to) real estate, financing, and some provider companies.

- S-Corp shareholder not paying reasonable compensation: This results in overstating the QBI coming from the S-Corporation and, therefore, overstating the deduction. This is not an uncommon source of letters from the IRS to the taxpayer and eventual changes to tax returns.

Key Takeaways

The Qualified Business Income (QBI) deduction is one of the most effective ways for business owners and freelancers to reduce their taxable income. By understanding the tax deduction, rules, staying organized with your financial records,you can make the most of this deduction and avoid costly mistakes at tax time. Keeping accuate check stubs can also help you accurately track your income and support your QBI deduction calculations.

Curious Mind Also Asks

1) What is QBI deduction?

The Qualified Business Income (QBI) deduction, often known as the Section 199A deduction, allows eligible self-employed individuals, sole proprietors, partnerships, and S-Corps to deduct up to 20% of their certified business income from their federal profits tax.

2) What is the benefit of a QBI deduction?

The QBI deduction allows eligible owners of pass-through entities such as sole proprietors, partnerships, S corporations, and positive LLCs to deduct up to 20% of adjusted gross income from their qualified business income, REIT dividends, and publicly traded partnerships.

3) Is QBI only for self-employed?

No, the QBI deduction is not limited to only self-employed individuals. If you earn cash from self-employment or run a small business, you are probably able to reduce your taxes with the QBI deduction. If you qualify, it is available to you whether you itemize deductions on Schedule A or choose the standard deduction.However, W-2 employees do not qualify for the QBI deduction on their wages.

4) How to maximize the QBI deduction?

One option is to contribute to a traditional retirement account. There are more opportunities to reduce taxable income in valuation, such as using itemized deductions with charitable contributions.

5) What is not included in QBI?

QBI does not include:

- Investment items, including capital gains and losses.

- Interest earnings should no longer be nicely allocated to barter or business.

6) Where is QBI shown on a tax return?

Qualified Enterprise Earnings Deductions on Line 13 of Form 1040. If you do not see it now, evaluate your entries for QBID/Form 8995. If you have not gone through the entire step, you may have overlooked the qualifying question.

7) Who is eligible for a QBI?

The QBI deduction may be best for taxpayers who earn income from certain pass-through corporations, not from traditional W-2 employment as employees. In the well-known, you may qualify for the QBI deduction even if you earn earnings from a sole proprietorship.

Also Check:

FAQ's

What are the new QBI rules?

+

Materially participate in an active qualified trade or business, and have at least $1,000 of QBI from that business.

Is QBI passive income?

+

QBI does not require clothing participation through the game owner. Thus, the interest is considered passive but qualifies for QBI functions. There are benefit limitations that affect eligibility for the QBI deduction.

What is the tax rate for QBI?

+

The tax rate for QBI is 20% deduction.