Wage garnishment is one of those payroll terms that seems to confuse employers and employees. It normally operates in situations where a court or government agency orders money to be deducted directly from an employee’s paycheck.

For business owners and payroll teams, what is wage garnishment needs to be understood. Even minor garnishment period gaps, deducting the wrong sum, or failing to submit paperwork on time can result in fines, penalties, and possible legal action against the firm.

Wage garnishment is especially problematic because there is no clear-cut way to do it. Different orders come with different processes, and payroll calculations need to be done carefully according to relevant state and federal laws. Having multiple garnishments at the same time complicates the process even further and requires prioritization while processing.

Due to these intricacies, knowledge of garnishment of wages is an important concept for ensuring compliance and avoiding costly payroll mistakes. Many individuals rely on a paystub creator to track their income, verify deductions, and maintain financial clarity, but what happens when a portion of your paycheck is legally withheld before it even reaches you?

In this guide, we will take a closer look at wage garnishment and how it works. Let’s dive deep into it.

What is Wage Garnishment?

Garnishment is a legal process in which a creditor collects some unpaid debts by withholding them directly from an individual’s paycheck.

The money is usually garnished by a third party and provided to the creditor. It is used as a last resort when a debtor has failed to make payments on a credit card, and the creditor has obtained a court judgment.

Garnishment involves the collection of unpaid debts through payroll deductions, allowing a creditor to request an employer withhold a specific percentage from an employee’s paycheck. In certain circumstances, though, the creditor must obtain an order from a court directing the employer to remit a portion of wages in satisfaction of the debt.

Certain government agencies have the authorization to garnish your wages without giving any notice, so it is possible that workers will not be informed about the deductions until they see them on their pay stubs. In the U.S., some agencies, particularly the IRS garnishment without a court order, especially in cases involving unpaid taxes or defaulted federal student loans.

Federal and state statutes limit the amount that may be withheld from an employee’s paycheck to make sure that the worker retains enough funds for essential living expenses like food, utilities, and medical care.

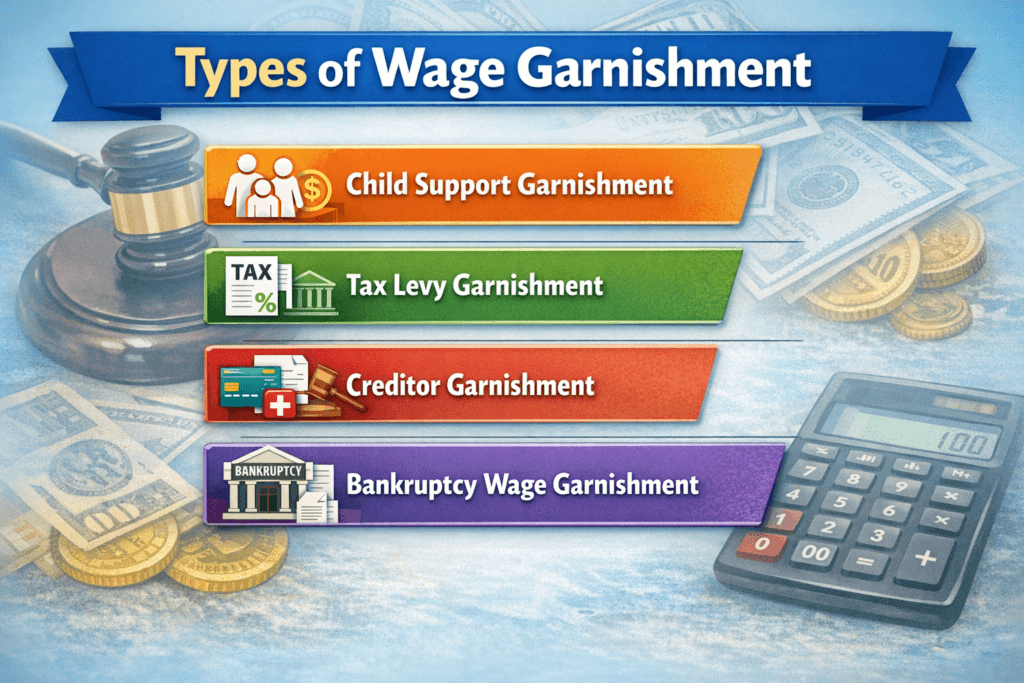

What Are The Types of Wage Garnishment?

There are 4 different types of wage garnishment, each of which has its own regulations and limitations. Below are the 4 common types:

1. Child Support

State or federal taxes place importance on child support payments to make sure there is well-being of dependent children. When a parent falls behind on payments, the court orders wage garnishments, which require the employer to deduct a percentage of the debtor’s earnings.

2. Tax Levies

In the U.S., government agencies like the IRS and state officials can garnish wages for unpaid taxes without notice. And a private creditor does not have to get a judgment to levy. The sum, which depends on the employee’s filing status and number of dependents, is forcing him to retain at least the federal minimum wage necessary for expenses.

3. Creditor Garnishments

When somebody defaults on an unsecured debt like medical bills and credit cards, a creditor can petition the court for a wage garnishment to collect on that debt.

4. Bankruptcy Court Orders

When a person with a tax debt files for bankruptcy, the court may issue an order restructuring their debts and mandating that a portion of that employee’s income be used to pay those debts. It can be withheld through payroll deductions to satisfy outstanding obligations with certain bankruptcy court orders.

Who Is Involved in Wage Garnishment?

Wage garnishment typically involves three parties: the creditor, the debtor, and the garnishee. Each has a significant part in ensuring that the debt is collected and the legal process follows.

1.Creditor

The creditor is the individual, corporation, or governmental entity that is owed money. This would be a court in many scenarios, the IRS, one state agency or another, or even a lender attempting to recoup their debt.

2.Debtor

The debtor is the one who owes the debt. In a work context, that is the employee whose paycheck is being garnished. The liability could result from back taxes, child support, student loans, or other financial commitments.

3.Garnishee

The garnishee is the third party that receives the order or writ of garnishment. It also holds the debtor’s property.

These roles can help employers and employees learn how to better work the garnishment process and minimize confusion or compliance issues.

How Does Wage Garnishment Work?

You can use a wage garnishment calculator to estimate how much might be deducted at each stage. Below is a working process of wage garnishment:

1. Debt Accumulation

You fall behind on payments, such as loans.

2. Legal Notice

You receive: warning letters and final demand notices.

3. Court Order

- A private creditor should get approval from the court.

- Government agencies can directly act.

4. Employer Notification

Your employer receives a garnishment order and is required to:

- Withhold a part of your wages.

- Send it to the creditor.

5. Wage Deduction Begins

The paycheck is reduced until:

- Debt is fully repaid.

- The garnishment is legally stopped.

How Does Wage Garnishment Work for Employers?

When an employer receives garnished wages ordered in the U.S., the employer must follow the law strictly to comply with federal and state laws. Below is the process:

Receive the Garnished Wages Order

Employers are required to be notified of wage garnishments via government agency directive, such as an IRS levy.

Notify The Employee

Some garnishing wages like tax levies can be enforced without prior notice, which mostly require employers to inform the employee.

Calculate Withholding Amounts

Employers should make sure that the garnishments comply with the law limits. Under the CCPA, the maximum amount can be withheld up to 60% for child support from garnished wages.

Process Payroll Deductions

The employer must modify the employee’s pay stub to reflect the garnished wages and send the deducted payments to the designated creditor.

Handle Multiple Garnishments

If an employee has multiple garnishments, certain debts take priority. For example, child support and student loans garnish wages, replacing other creditor garnishment.

Respond To Legal Inquiries

Organizations should comply with federal and state laws regarding garnished wages. In case an employee disputes the garnishment, the employer might receive additional court communication that aligns with the terms of withholding.

How Do Wage Garnishment Limits Vary by Debt Type?

Child support and alimony result in the largest deductions; federal student loans and unpaid taxes each have their own restrictions. Below is a breakdown of how much can be garnished for various types of obligations:

- Consumer debts: Consumer debts, like medical bills, are up to 25% of disposable income, which might be garnished.

- Unpaid taxes: IRS determines garnishment amounts based on filing status and number of dependents, making sure that the employees retain at least the minimum income threshold.

- Child support and alimony: 50% of disposable income might be garnished if the employee supports another child. If payments are over 12 weeks overdue, an additional 5% might be deducted, bringing the total garnishment of 65%.

- Federal student loans: The government can garnish up to 15% of disposable income without a court order for defaulted student loans.

How Much of Your Wages Can Be Garnished?

If your wages are being garnished, federal law gives you some protection under the Consumer Credit Protection Act. This law restricts the amount of take-home pay that can be garnished based on your income and the type of debt owed.

For private debts, the amount garnished in a single pay period may not exceed either 25% of your take-home pay or, at this level. Take-home pay minus 30 times the federal minimum wage; whichever is less. However, if your take-home pay is 30 times the federal minimum wage or less, currently $750 a week, garnishment is usually off-limits.

Unless federal law requires or permits a certain amount to be garnished, state laws may impose further limitations on wage garnishment. Furthermore, certain federal or state benefits (e.g., Social Security Administration Benefits) may remain entirely exempt from garnishment.

The garnished amount depends on the debt type and applicable laws. Below is the breakdown:

General Federal Limits

- Up to 25% of disposable income

- The amount exceeding 30x the minimum wage

Student Loan Garnishment

- Upto 15% of disposable income

- Should leave at least a minimum protected income

Major Protection Law

- Limits how much can be garnished

- Prevents termination for garnishment

How Can I Stop a Wage Garnishment Immediately?

Below are the steps to stop a wage garnishment immediately:

1. Contact Your Creditor

Talking with your creditor can lead to a resolution. Explain your financial situation, and also ask if they are willing to work on a payment plan.

2. File an Exemption Claim

You might qualify for an exemption, which can reduce the amount that is garnished. Filing a claim requires proving that the garnished amount is affecting your financial hardships.

3. Seek a Legal Representative

When you hire an attorney, it is the most efficient way to stop wage garnishment quickly.

4. Negotiate a Settlement

You might have the option to negotiate a settlement with your creditors for a huge payment that is less than the total debt owed.

5. Request Hearing

If you believe that the garnishment is incorrect, you can request a hearing in court to challenge it. This allows you to showcase your case, and if it becomes successful, it might result in the garnishment being terminated.

Pro Tip: Before downloading, preview the free pay stub template to ensure it includes all key details like employee info, earnings, deductions, and net pay so you can avoid edits later and save time.

Who Can Garnish Wages Without Notice?

Various entities can garnish wages without notice:

- Creditors

- Government agencies

- Student loan providers

- Homeowner’s application

- Child support and alimony enforcement agency

Can Credit Card Companies Garnish Your Wages?

In various cases, credit card companies cannot directly take money from your wages, but they can take legal action in various situations, such as:

- Credit card companies cannot directly take your wages

- They must sue and win a court judgment

- They can get a wage garnishment order

How Can StubCreator Help You with Wage Garnishments?

With detailed pay stubs that show your gross pay, deductions, taxes, and net income, StubCreator helps you understand your paycheck. Making it simpler to estimate how much of your income is likely to get garnished.

This also keeps your financial records in order and allows you to look over garnishment calculations or budget with your disposable income.

Key Takeaways

Federal law limits the proportion of your wages that can be garnished, while certain benefits and levels of income are exempt. State laws can offer even greater protections. By regularly examining your pay stub at least once a month, you can stay on top of how much money you are making for the work that you do and how many subtractions might occur, as well as more accurately estimate what the garnishment amount might be.

With the return of stricter policies in 2026, especially around student loans, it’s more important than ever to stay informed and proactive.

People May Also Ask

1) What does garnish wages mean?

A wage garnishment is an official court order that directs an employer to collect funds from an employee to fulfill various financial obligations, such as child support.

2) One consequence for defaulting on a loan is to have your wages garnished. What does this mean?

This means that wage garnishment can occur without a court order, especially for federal debts. The federal government can garnish as much as 15% of disposable wages, and borrowers get a notice before garnishment occurs. State laws also differ; some states prohibit garnishments altogether.

3) Your employer withholds money from each paycheck. What is this money used for?

This money is used for paying federal, state, and local taxes, along with FICA taxes.

4) How to stop a garnishment?

You can file a claim of exemption with the court to protect your income from garnishment, or file for bankruptcy, which results in an automatic stay, or pay the debt in full.

5) Can student loans garnish your wages?

Yes, student loans can garnish your wages if you’re in default.

6) What does it mean to garnish wages?

Wage garnishment is a legal process in which part of your paycheck will automatically be withheld from you by your employer to pay off a debt, such as unpaid taxes, before you even see the money.

7) Can debt collectors garnish wages?

Yes, debt collectors can garnish wages, but only after suing you and obtaining a court judgment.

8) How does wage garnishment work?

Wage garnishment is the legal process by which a court or government agency orders your employer to withhold part of your salary toward paying off the debt. The deducted sum goes straight to the lender until the loan is fully paid off.

9) Can a credit card company garnish your wages?

Yes, credit card companies can garnish your wages, but they cannot do it directly.

10) Can a creditor garnish my wages after 7 years?

Yes, a creditor can garnish your wages after 7 years if it is a valid, renewed court judgment that lasts 10 to 20 years.

11) How much is child support in NY?

Child support in NY standard percentages is as follows: 17% (1 child), 25% (2 children), 29% (3 children), 31% (4 children), and 35% for 5 or more children.

12) Can a debt collector garnish your wages?

Yes, a debt collector can garnish your wages but only after it has won a lawsuit and received a court order.

13) How to check wage garnishment balance?

For a payment status, you’ll want to reach out directly to the creditor for the accurate figure, including interest.

14) What are disposable earnings?

Disposable earnings are those you have free to spend once all taxes, along with other mandatory expenses (such as social security contributions), are deducted.

15) Can unemployment be garnished?

Yes, unemployment benefits can be garnished, mainly for child support or state tax debts.

Also Check:

Payroll Card vs Direct Deposit

FAQ's

Can the IRS garnish your wages?

+

Yes, the IRS can garnish your wages without any court order to pay unpaid taxes.

Can a collection agency garnish your wages?

+

Yes, a collection agency can garnish your wages, but only after it sues you and wins a lawsuit and gets a court judgment.

How to find out who is garnishing my wages?

+

You can instantly look through your pay stubs for details on creditors or simply call up your employer’s HR department, since they are officially obligated to supply the garnishment order.

Can IRS garnish wages?

+

Yes, the IRS has very potent tools in its arsenal, like garnishing wages without a court order. They can garnish a portion of your wages, typically up to 25% of your disposable income, directly from your employer.

How much can child support take from your check?

+

Child support takes between 50% and 60% of a parent’s disposable income, which depends on whether they are supporting another spouse and if they are behind on payments.

Can Social Security be garnished ?

+

Social Security Administration benefits are protected from garnishment for private debts like credit cards or personal loans. However, they may be garnished for certain obligations.