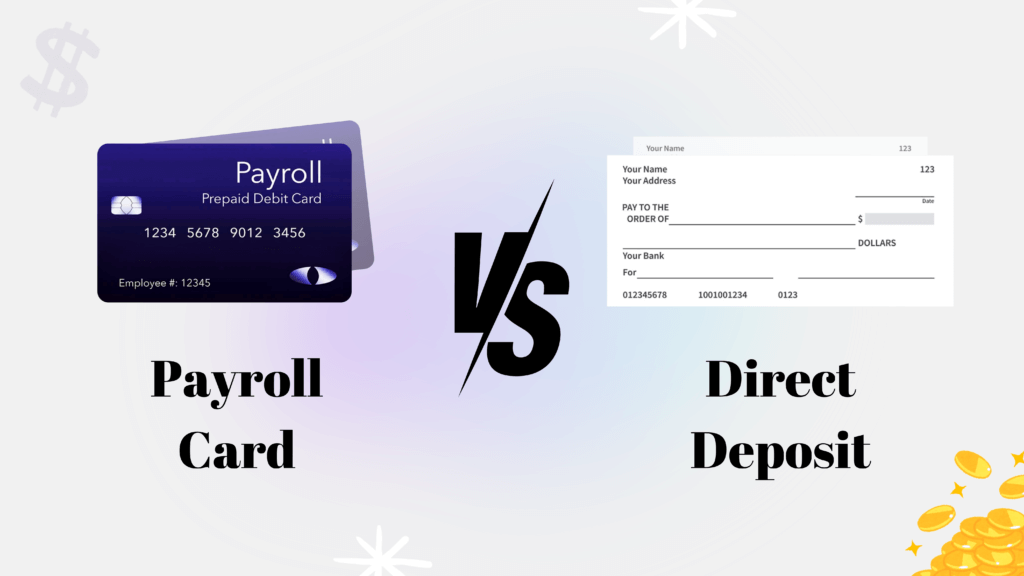

When comparing direct deposit vs payroll card, both are common employee payment methods but work differently. Direct deposit transfers money to a bank account, while payroll cards carry salaries on a prepaid card for those without a bank account. Knowing the advantages and disadvantages helps choose the best method.

In the business world, payroll card vs direct deposit lies between the fees, with the wage distribution methods and accessibility of salary. Both options are convenient and paperless, are feasible, but they have different benefits and drawbacks. Regardless of the method chosen, businesses often utilize a free check stubs maker to ensure accurate record-keeping for every transaction.

In this guide, we will be covering all the topics about direct deposit vs payroll card, and this will be your one-stop blog where you will get to know about everything regarding payroll card & direct deposit.

What is a Payroll Card?

A payroll card (paycard) is a prepaid debit card that employers use to pay salaries, and employees use to access their earnings digitally without using a bank account. Employers directly send their employees’ earnings to prepaid payroll cards, and then they can withdraw funds to make purchases.

When you compare a payroll card and direct deposit, it is the simplest way to understand how the former works. Both options allow holders to access their earnings, make purchases in stores, and transfer funds to other accounts. The main difference is that a payroll card is not linked to a checking account.

They both are the best options for employees who do not have access to a traditional bank account. Moreover, they offer an alternative to paper checks, which have various drawbacks in terms of payroll security.

A payroll card comes with fees for withdrawal and balance inquiries, which can add up over time and affect the employee’s earnings.

How does a Paycard Work?

Employers create and implement a payroll card program with a third-party administrator. They enroll employees choosing this option, and the provider issues payroll cards. This method of payment is linked to a bank that permits the transfer of funds; this link is between the paycard vendor and the bank, not between the employee and the bank.

Instead of receiving a paper check, employees can use a paycard to obtain cash and monthly pay expenses up to the limit of their wages. Paycard works like a person using a debit card while purchasing something or paying bills. A paycard allows the holder to use only the funds loaded on it.

Employees can access funds from the payroll card directly. Money can be attached to the same paycard with each employee’s pay cycle, so it is necessary only to provide a single card during the life cycle of their employment.

What is Direct Deposit?

Payroll deposit, commonly known as direct deposit, is a payment method in which the funds are directly deposited into an employee’s bank account. It is an electronic funds like a payroll card, which is more convenient than a paper check.

This is the most common method of distributing salary and is an important part of payroll administration. To set up direct deposit, employers need bank accounts and routing numbers. Before finalizing these systems, it is often helpful to preview a US-compliant pay stub sample template to see how the transaction details will look on the official record. After that, the funds can be effortlessly deposited on paydays via the Automated Clearing House network.

Once an employee receives funds in their savings account, they can use them immediately without having to visit the bank branch. This will reduce the risk of stolen payments and will remove any delays that may occur when banks are on holiday.

Direct deposit allows employees to manage their finances in a more efficient manner. They can set up automated bill payments. Employers can be much more efficient with payroll processing as direct deposit allows for reduced operating costs and improved automation. To ensure these automated payments are backed by professional documentation, Visit StubCreator.

How does Direct Deposit Work?

Direct deposit funds are deposited into a recipient’s account directly through a digital network. For the funds to be transferred from the payee, the recipient must provide name of the bank, account number and the bank’s routing number as the person making the deposit. Alternatively, they might provide a voided check that has the same information on it.

Setting up a direct deposit can take some days. Once the depositor has all the information, funds are transferred digitally and are deposited into the recipient’s bank account at midnight on the payment date. Funds automatically get cleared through ACH and are immediately available, eliminating the need for a bank hold.

This method is used to transfer employees’ funds, payments from retirement accounts, and benefits like Social Security. The payment of bill are made using direct deposits from debtors to creditors.

Most of the direct deposits are done using bank accounts as well as automated clearing houses. These payments can be done by using net banking and by transferring through phones.

For example, if a family member wants to directly send money to another member, they need to have the other person’s email address or contact information. The recipient provides the transfer company’s bank account information. Once the money is transferred, it is deposited into the payee’s account.

Also Read: Bi-Weekly vs Semi-Monthly Pay

Pros and Cons of Payroll Card

A payroll card has many benefits. We have shown the main pros and cons of it:

Pros of Payroll Card

- No need for a bank account: Payroll cards are the perfect choice for employees who do not have a bank account.

- More convenient: A paper check takes up a lot of time to be delivered, and employees need to deposit it to gain access to their funds.

- Cost-effective: Paper checks require resources and effort to be delivered to employees.

Cons of Payroll Card

- Payroll card use fees: Many pay cards charge fees when withdrawing cash from ATMs. There are potential fees associated with purchases, inquiring about balance, and other circumstances, which can reduce your net pay.

Pros and Cons of Direct Deposit

Below are the pros and cons of Direct Deposit:

Pros of Direct Deposit

- Security and convenience: Direct deposit is a common method of distributing salaries quickly, directly to employees’ accounts. The funds are transferred via a secure banking system, which reduces the chance of mistakes while providing recipients instant access to their salary.

- No needless fees: There are fees associated with using a direct deposit bank account; they are lower than if you were to use a payroll card.

Payroll Card V/S Direct Deposit: Key Differences

| Feature | Payroll Card | Direct Deposit |

| Payment speed | On payday | On payday (sometimes earlier) |

| Money access | Card swipe, online purchase | Online banking, transfers |

| Security | Secured with a PIN | High security with bank protections |

| Convenience | Good for employees | Easy to manage finances |

| Bill payments | Limited options | Online bill payments |

| Best for | Unbanked employees | Employees with bank accounts |

Which Payroll Method is Best For Your Business?

Choosing the best payroll method for your business depends on various factors:

- Accessing the bank systems: If an employee does not have a bank account, they will not be able to receive their earnings via direct deposit.

- Payroll processing costs: Direct deposit lowers payroll processing costs as compared to distributing paper checks.

- Turnover rates: If you work very often with a contract worker, payroll cards may be better suited.

Why Every Payment Method Requires a Pay Stub?

Each payment method requires a paystub because it becomes an official record of how many employees are being paid. Below are some methods that can be used:

- Legal proof of payment: A paystub shows evidence that an employee was paid correctly. It shows gross pay, deductions, and net pay. Protects both the employer and the employee in case of disputes.

- Transparency: Employees need to know how their pay was calculated. Stubcreator’s instant paycheck stub maker shows hours worked, taxes deducted, benefits, and net pay.

- Compliance: Tax authorities require accurate payroll records. It helps them with income tax, social security, and other statutory deductions.

Key Takeaways

Direct deposit is ideal for workers with bank accounts who want fast, automatic payments and easy access to their money with no extra fees. It offers better control, smooth budgeting, and seamless integration with banking services.

On the other hand, payroll cards are a practical option for unbanked or underbanked employees. They eliminate the need for a bank account and provide quick access to wages, though users should be mindful of potential fees and limited banking features.

FAQs

1) What is the difference between direct deposit and a payroll card?

The main difference between direct deposit and a payroll card is in the path the employer takes to send earnings and employees’ access to them.

2) Can I switch from paycard to direct deposit?

If you change jobs, you can continue to use the card via your next employer, and you can change from your payment method to direct deposit at any time.

3) Can I withdraw cash from a payroll card?

Employees have access to their money from their card and can use it as a debit card. Employees can use a payroll card to withdraw cash from an ATM or shop online.

4) Why do banks issue payroll cards?

A payroll card is a prepaid card that employers can use to pay employees’ wages. Payroll cards allow employers to pay employees who do not have bank accounts.

5) What is the 2/3/4 rule for credit cards?

Applicants are limited to two new cards in 30 days, three new cards in 12 months, and four new cards in 24 months.