What Is FIT on My Paycheck? A Complete Guide

Posted On: Dec 20, 2025

Instant Delivery

Get your first pay stub free ($4.99 value) every year, per user and company. Standard pricing applies thereafter.

A free paystub generator is an online tool that helps small to medium businesses, as well as employees, self-employed, and freelancers, to generate professional-looking and accurate pay stubs easily.

Each pay stub includes detailed payroll information, which establishes transparency and accessibility. This offering streamlines payroll management and optimizes efficiencies for anyone in need of compliant, best paystub solutions.

These features make creating check stubs quick and simple. Each one is designed to save time while keeping it accurate and 2026 compliant.

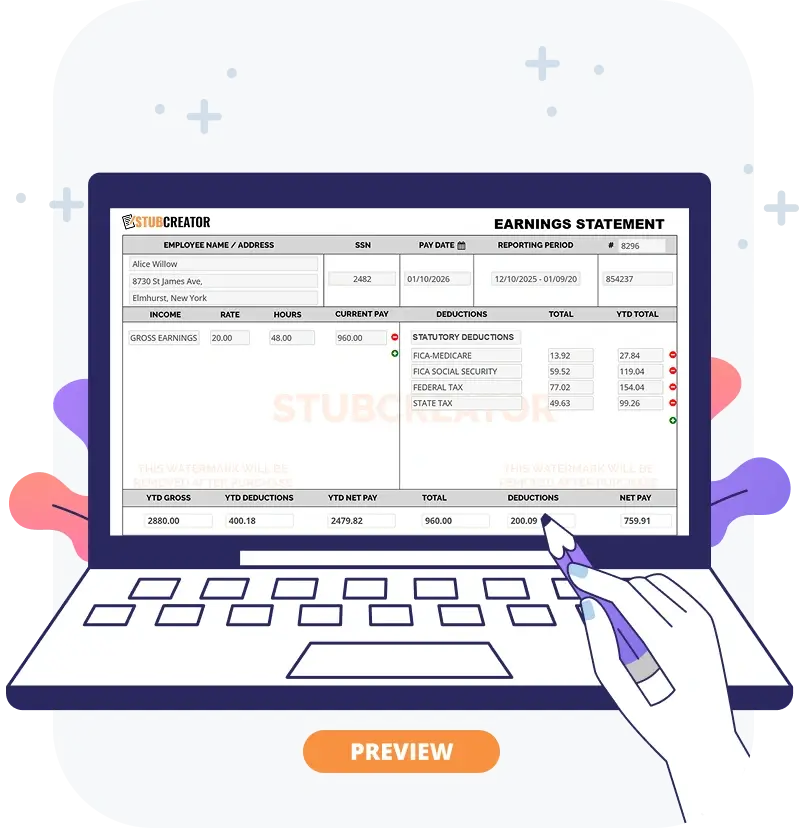

Simplified UI and hassle-free paystub creation. Just enter details easily with a simple 3-step process, creating paystubs online quickly, even for first-time users.

Create and download your first free paystub instantly without signing up or entering any payment details. There are no hidden fees.

Up-to-date federal, state, and local payroll tax compliance for 2026, with automatic & precise calculations for net earnings, deductions, and withholdings.

Catch and fix mistakes in your pay stub if you have made any mistakes while creating it. Make free corrections at no extra cost while using this free check stub maker.

Create professional pay stubs suitable for proof of income, employee income verification, loan applications, and more.

Tax Accuracy

Our pay stub calculations follow the 2026 IRS tax tables, including IRS Publication 15-T, FICA limits, and the 50 states of the USA tax rules to ensure accurate withholdings. The paystub generator free tool ensures correct calculations for all earnings, taxes, and deductions, and helps employers comply with federal, state, and local regulations.

Data Privacy

Your payroll data is protected with 256-bit SSL encryption and secure systems. We do not sell, share, or disclose your personal or business information.

Instant Preview

In this check stub maker, you can preview your complete pay stub before downloading a high-quality PDF. The final document reflects exactly what you see during the preview step.

Expert Review

Payroll formulas are verified by expert accountants and aligned with standard accounting practices to support accurate pay stubs for employees, freelancers, W-2, and 1099 workers.

First Paystub Free Every Year

Get your first paystub worth $4.99 totally free while using StubCreator online. You don't need any subscription or dedicated payroll software to generate free pay stubs.

Templates & Customization

Select from various detailed pay stub template options to offer a reliable option for your organization. Preview the layout by downloading a template, then generate your pay stub to customize it according to your payroll details. You can customize the colours of your template that fit with your company branding.

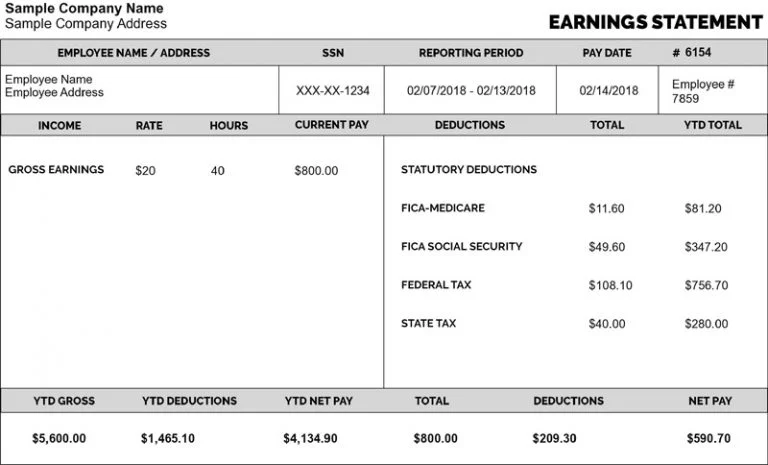

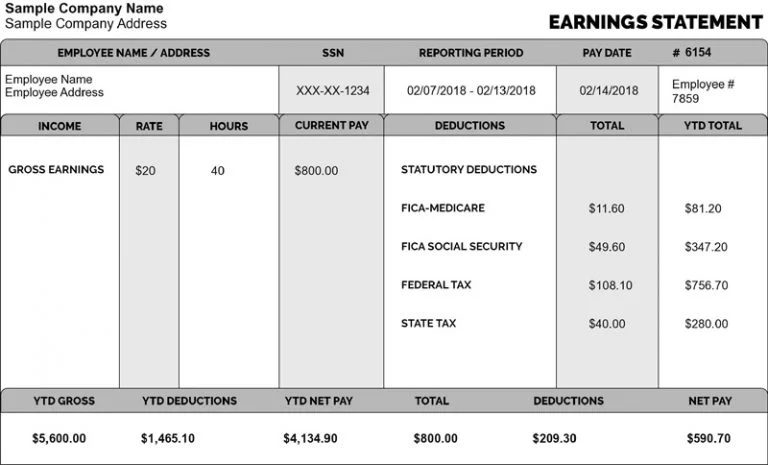

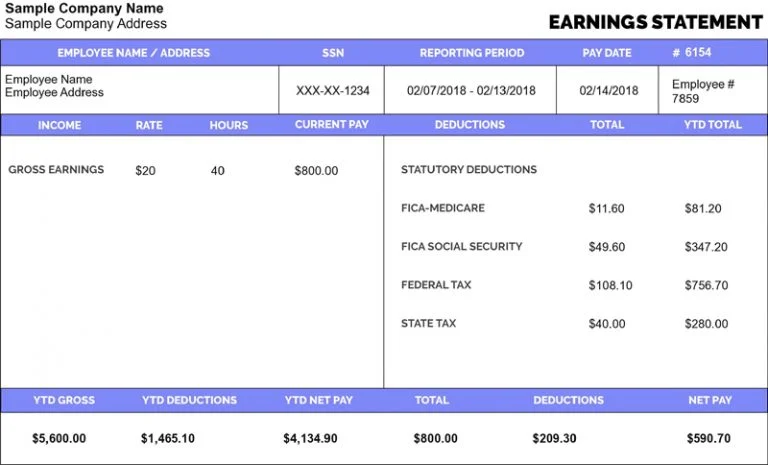

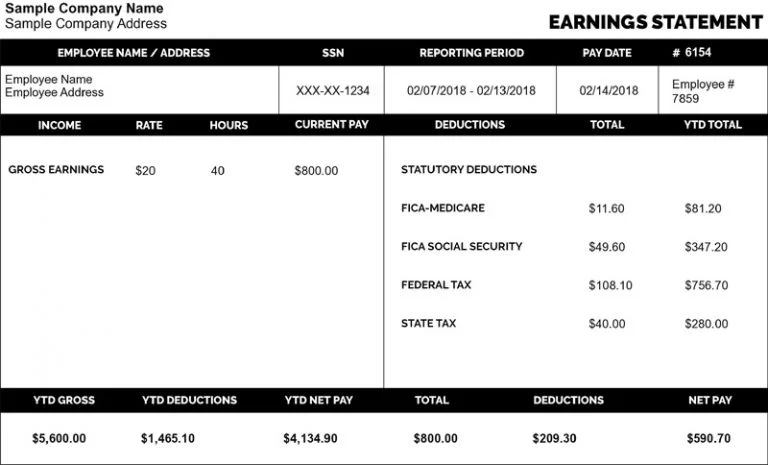

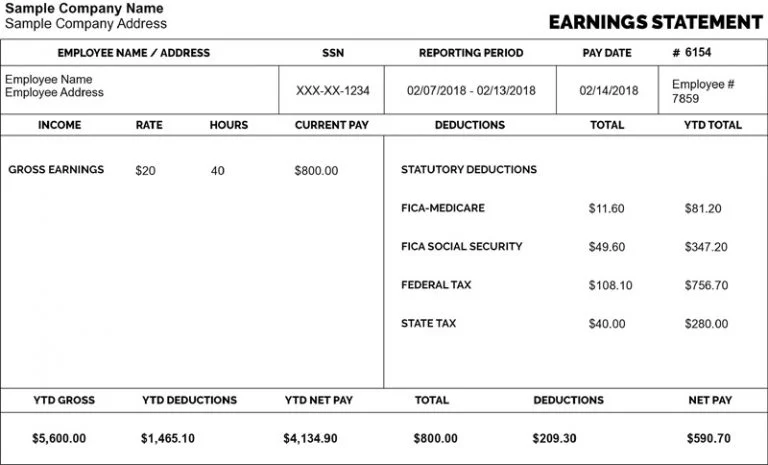

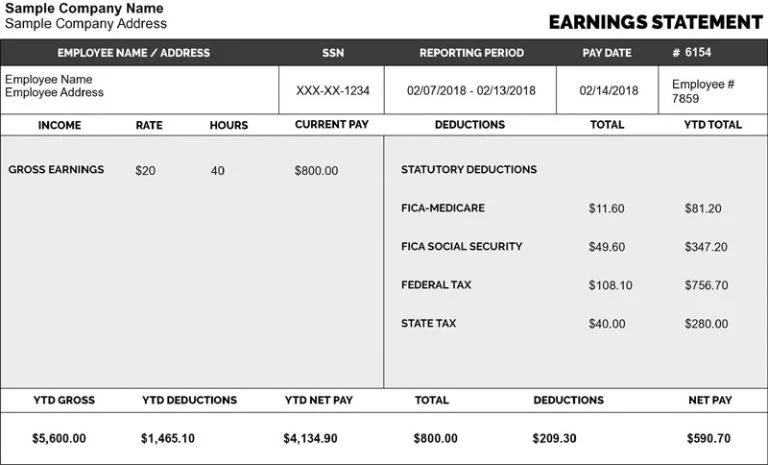

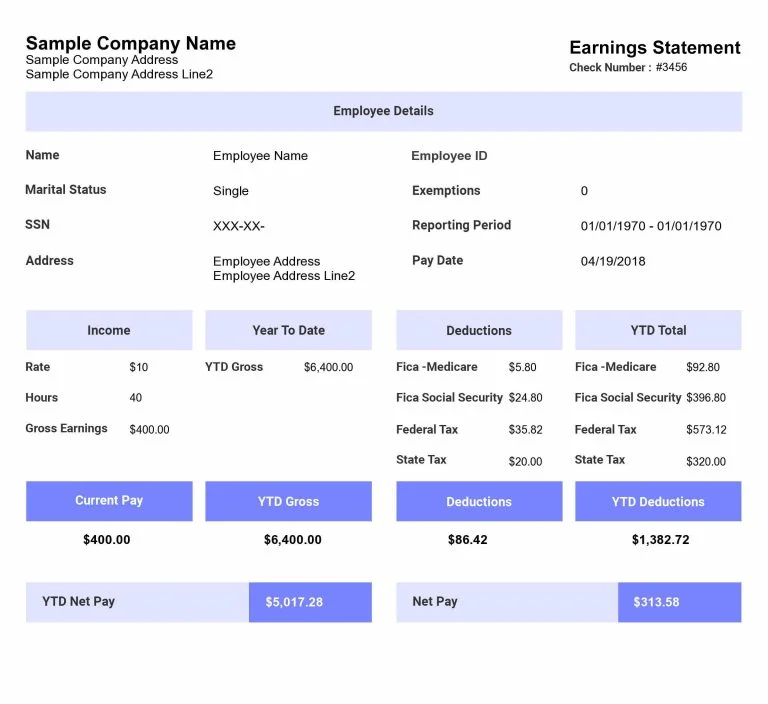

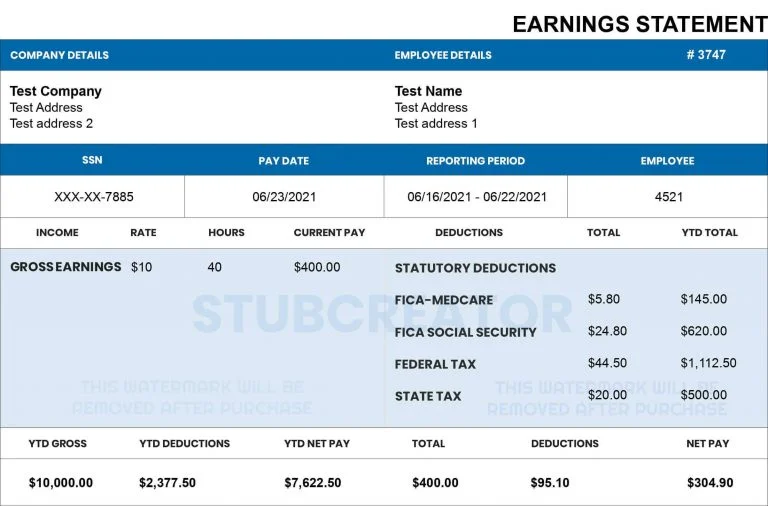

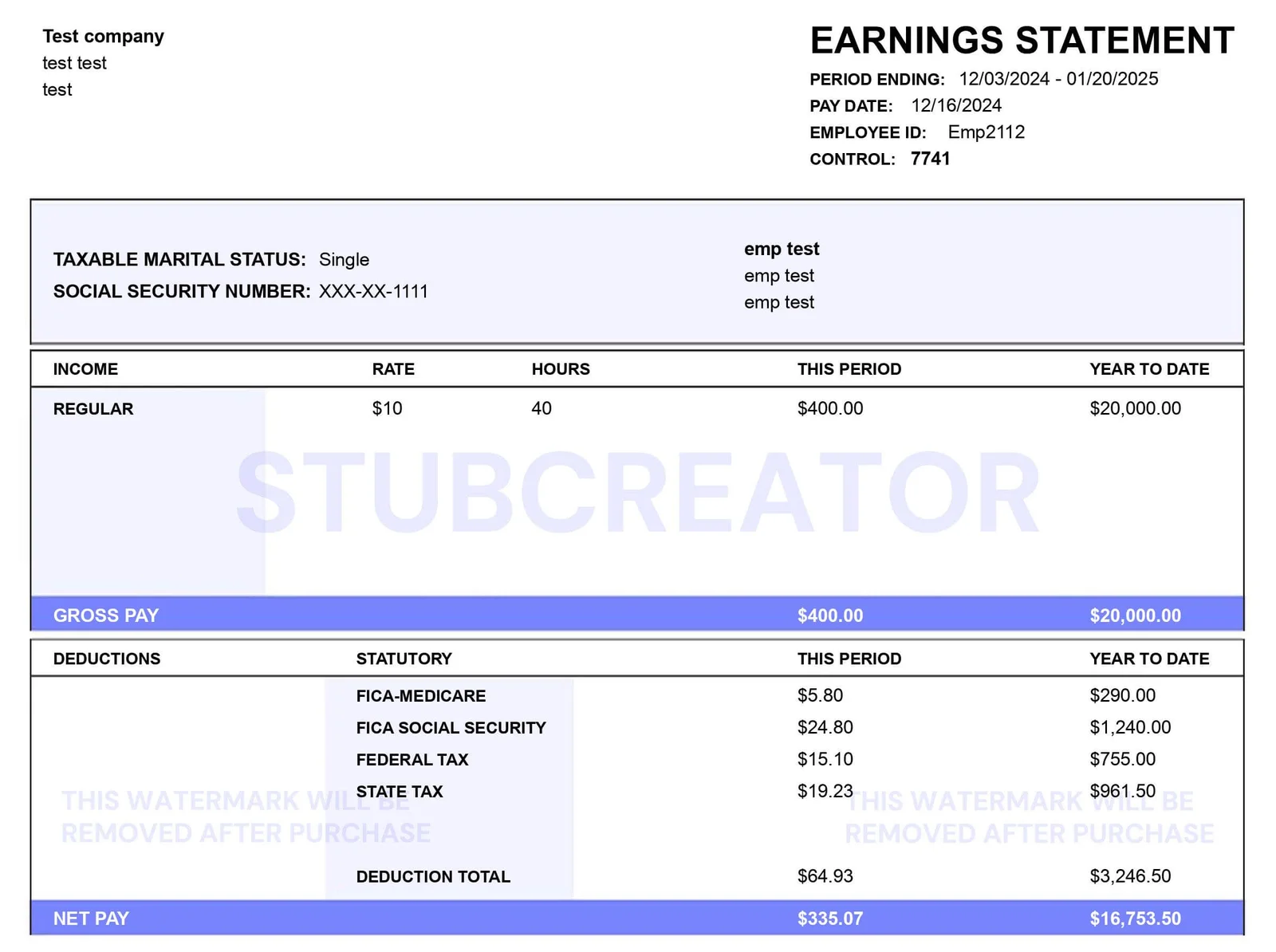

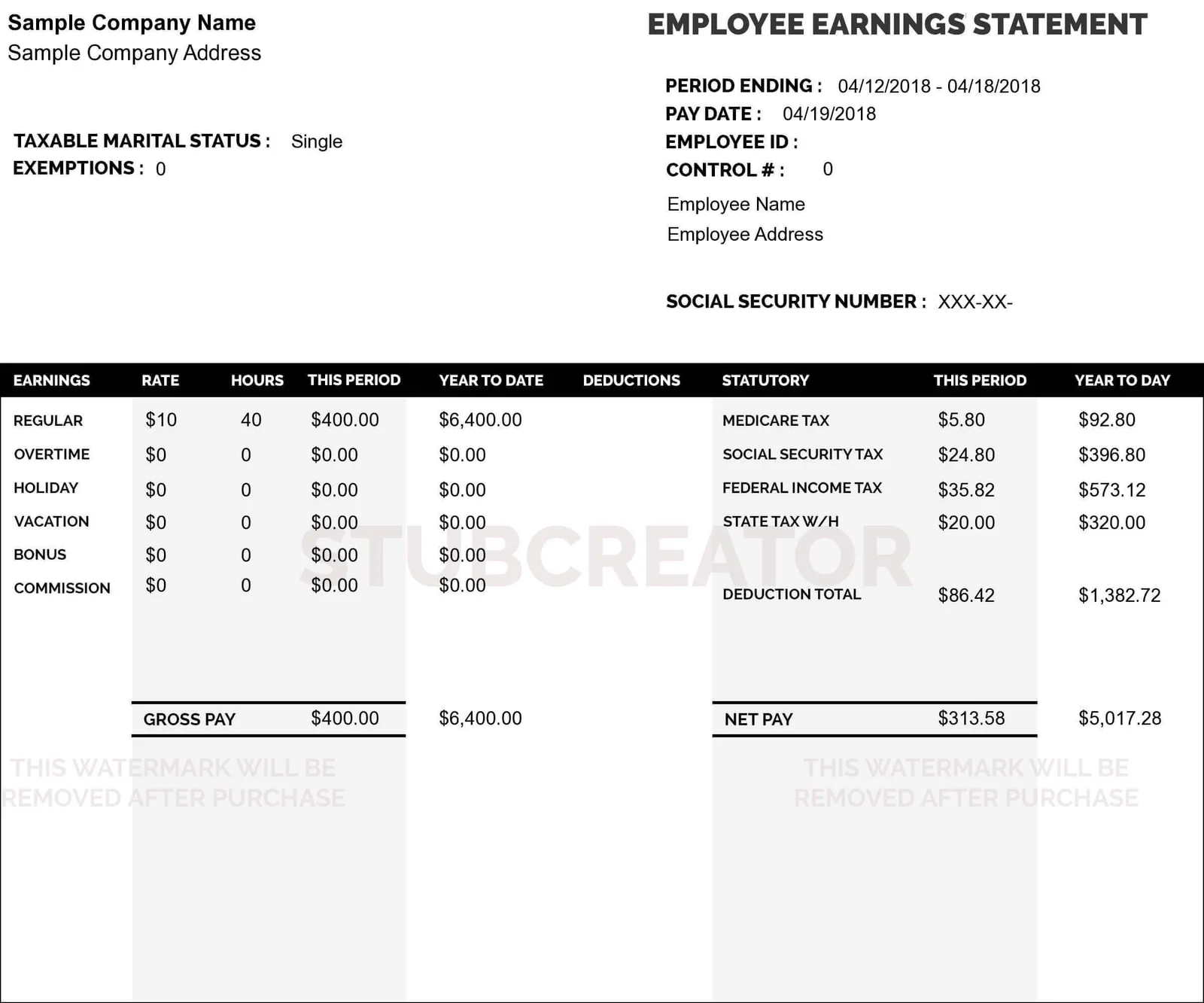

An employee pay stub is an earnings statement or paycheck stub with information about the salary details, including total earnings, deductions, and net pay for a specific pay period. The paycheck stubs ensure that you have a detailed record of payroll information for understanding your earnings, planning your budget, and making important financial decisions.

As an individual or employee, a pay stub can help you in many real-life scenarios. Here are the most common scenarios where you will need one:

Beyond these, pay stubs also come in handy for disability claims, visa applications, and for freelancers, independent contractors, and small business owners who need a reliable way to show proof of income.

Running a small or medium-sized business means handling too many operations, and payroll is one of those tasks that can quietly waste more time than it should. Without a reliable payroll system in place, things tend to slip through the cracks. Here are some of the most common pain points SMEs deal with:

Switching from paper payroll to electronic pay stubs, one of the smartest choices by the management. This saves time, reduces storage costs as well as ensuring a smooth payroll process.

No need to print and physically distribute pay stubs to every employee.

Eliminates the need for physical filing of records that are difficult to manage and easy to lose.

Employees can access their pay stubs from anywhere, anytime without requesting copies.

Digital records are easier to organize and search if the IRS Department ever requests them.

A fake pay stub contains incorrect income figures, manipulated tax calculations, or information that doesn't match actual payroll records. It is often created by manipulating documents with image editing software.

Your job could be at stake if discovered by your employer

Your loan application will be rejected

This could be considered as committing fraud or a federal felony

A maximum of 5 years in prison possible

Financial penalties can reach up to $1 million

Mismatched IRS table tax figures

Oddly rounded pay amounts that look unrealistic with regular payroll calculations

YTD totals that don't add up across pay periods

Inconsistent fonts, incorrect calculations or unprofessional formatting

Misaligned columns, or poorly aligned numbers

Many tools produce inaccurate or fraudulent pay stubs that are entirely useless and in some cases illegal. StubCreator's pay stub generator eliminates this risk by producing fully verified paystubs.

Generating pay stubs is essential for businesses and independent contractors, as they serve as official proof of income, tax deductions, and employment records. Our free paystub creator simplifies the time-consuming and costly process by delivering quick and reliable results.

With a Paycheck stub generator, all it takes is a few minutes to create pay stubs online for free.

You can check and select these add-on features to customize your pay stub.

As a small-business owner or freelancer, professional pay stubs are necessary not only for tax filing but also to secure loans and maintain transparency in your finances. The pay stub generator free tool is very valuable for small business owners and independent contractors to grow by streamlining payroll processes and improving efficiency.

The following entities need a pay stub generator:

Employees use pay stubs for several reasons. A paystub shows how much you earned and what was deducted. It is used as proof of income when applying for a loan, renting a home, or tax filing. Employees can easily generate their own check stubs using a free paystub generator without payroll knowledge. A free paystub maker can help you create a paystub to calculate your income and tax details.

Paystubs show when employees were paid and how much they received. Paystubs are also useful to track employees’ income & deductions. A paystub creator helps employers to generate accurate paystubs quickly, maintain consistent formatting and appearance across pay stubs for multiple employees, and keep payroll records organized.

Freelancers and entrepreneurs do not have steady incomes. So, they can create instant proof of income by using pay stubs maker. For entrepreneurs who are paying themselves, accurate payment stubs serve as valid documentation. It also helps showcase income consistency across different clients or business earnings, making financial verification easier.

Accountants often work with businesses that do not have a payroll system. You can utilize a free paystub maker, which will help to make detailed records to verify all incomes and deductions.

Ride-share drivers, delivery drivers, and other gig workers who work on an hourly basis or work part-time often do not receive formal pay stubs from their workplaces; that’s where a pay stub creator helps to get proof of income for renting.

A free Paystub generator allows small businesses to record the pay of every employee without doing any extra busy work! It facilitates the owners and lets them make clean records with formatted pay, which will fulfill all your requirements.

Monitoring employee pay stub data in Excel sheets is challenging, especially for mid-sized organizations. A free pay check stub generator simplifies the process that guarantees accuracy in mass payroll.

Those who are self-employed do verify income with current pay stubs when applying for loans, or can use these documents to record their income, expenses and deductions. Pay stubs are specifically created to include key information needed for income verification.

Payroll amounts are taken from your employees’ paychecks before they see the final amount as net pay. These payroll deductions apply selected expenses which include taxes, benefit schemes and savings initiatives (such as retirement contribution). While using an online free paystub generator you need to be aware of tax compliance laws and obligations when it comes to payroll processing.

Common payroll deduction examples include:

The FIT taxes are applied to wages, bonuses, and tips, which the entire US workforce needs to pay unless they fall in a lower income slab that is exempted. These taxes are computed using IRS guidelines for the purpose of accurate withholdings.

State and local taxes like CASDI in California, PFL in New York, and state income tax are also based on the location of the employee, not the employer.

Employees are required to withhold a portion for Social Security and Medicare from every paycheck. Employees may also choose to contribute to health savings accounts or flexible spending accounts.

These could be standard or Roth 401(k) plans and USA pension contributions. Both employers and employees can even pitch in, to ensure long-term financial security and retirement health.

If applicable, dues are deducted for employees covered by a union agreement. Such dues help finance various union activities and collective bargaining on behalf of all covered members, including their program of training.

StubCreator is an online paystub generator for 2026 tax standards. It compiles everything, conveniently calculates all these taxes; federal, state and local taxes as well as FICA (Social Security & Medicare tax) and ultimately generates accurate and compliant pay stubs with a single click.

There are also allowances for specific withholdings, such as health insurance premiums, retirement (401k) contributions and wage garnishments. If you need complete control over tax calculations, use the Custom Paystub Generator to configure deductions for absolute accuracy.

Our Paycheck stub maker will apply accurate 2026 rates to all 50 states in the United States

Note: Our tool is updated for the 2026 tax year, including the new inflation-adjusted Federal income tax brackets and the updated Social Security wage base of $184,500.

Create accurate pay stubs in just a few easy steps.

Get your first pay stub free every year and pay only from the second pay stub onwards!

Is it legal to use a pay stub generator?

+

Yes, a pay stub generator is legal as long as the information provided is 100% accurate and used for legal documentation purposes. However, it’s important to follow federal and state laws to make sure your pay stubs meet all legal requirements.

Can I create my own pay stub?

+

Yes, you can generate your own pay stubs whether you are an employee, self-employed, a freelancer or a contractor. However, you need to take care, all wage, deduction and tax info needs to be accurate and understandable!

How are fake pay stubs detected?

+

Fake stubs are identified based on the lack of details, inaccurate tax calculations, or information that does not match up. Since false pay stubs easily mix up with real ones that follow payroll regulations and somewhere, the number does not seem to add up, it becomes an obvious distinction.

Is StubCreator a legal pay stub generator?

+

StubCreator is an online pay stub generator that takes care of all the compliance requirements because StubCreator uses only trusted payroll formulas to generate your professional paystub.

How to generate a pay stub for free?

+

To generate pay stubs for free, simply enter your company details and wage details into our free paystub maker, preview the document and download your first paystub at no cost.

What's the ideal free paystub generator?

+

The ideal paystub maker tool is one that is updated for the 2026 IRS 15-T tables, offers 100% secure SSL encryption, and provides a professional PDF format for W-2 and 1099 workers.

Can I use this payroll tool for Canadian employees?

+

No, this specific tool is calibrated for US current tax laws. For Canadian payroll, you must use our dedicated Canada Paystub Generator. It is specifically designed to handle CRA requirements, provincial tax rules, CPP, and EI calculations accurately.

Do I need any payroll or accounting knowledge to use this tool?

+

No, you don't need any payroll or accounting knowledge to use this tool. Simply enter your information and create your paystub in 3 simple steps.

Is your 2026 Social Security calculation updated for the new wage base?

+

Yes. The Social Security (OASDI) tax wage base for 2026 is $184,500. Then the generator will stop taking out 6.2% from an employee's payroll when that worker’s YTD earnings match this number.

Are these stubs accepted as proof of income by banks or landlords?

+

Generally, yes, if you have provided the information accurately and honestly.

What information do I need to get started?

+

You will need Company info, employee info, pay info, etc, to get started with paystub creation.

Does your generator support the new 1099-NEC $2,000 reporting threshold?

+

Yes. The platform's 1099-NEC forms reflect the 2026 rule change that hiked the reporting threshold to $2,000 from $600.

How are the new 2026 Federal Income Tax Brackets applied?

+

The system applies the 2026 brackets, adjusted for inflation. This means that the 10% rate now applies up to $12,400 for single filers, and the standard deduction has been revised to be $16,100 (for Single) and $32,200 (Joint).

Does the generator include the new 2026 "Trump Account" (TA) employer contributions?

+

Yes. Employers can deposit up to $2,500 in an employees’ “Trump Account” (TA) beginning on July 4, 2026. You can enter these as tax-free employer contributions in the tool, and they will be coded correctly for W-2s.

Posted On: Dec 20, 2025

Posted On: Apr 01, 2026

Posted On: Mar 10, 2026